Business Strategy 30 March 2026

Why the Traditional CPG Value Equation Is Breaking and How Leaders Must Respond

The CPG growth model that delivered decades of value is no longer sufficient in a fast-changing, fragmented market environment.

Price-led growth has reached its limits, while volume growth increasingly depends on deliberate penetration strategies.

Capital-intensive industrial assets remain essential but are no longer the primary source of competitive advantage or shareholders’ returns.

CEOs recognize the need to rethink business models. Yet legacy structures and investment footprints complicate the transition.

Sustained value creation will require combining penetration led growth with new business models that rebalance assets, insight, and adaptability.

Sevendots, Rome

8 minute read

Why CPG’s growth challenges are structural, not cyclical

The CPG growth model that delivered decades of shareholder value is no longer fit for today’s market. Price-led growth is reaching its limits, volume growth is stalling, and capital markets are signaling that traditional scale is no longer enough.

Large Consumer Packaged Goods (CPG) companies are facing a growing structural challenge. In an environment characterized by accelerating change, fragmented consumer demand, rising competitive intensity, and increasing channel complexity, many CPG leaders are finding it harder to sustain volume growth. This difficulty is now cascading through the value equation: margins are under pressure, price increases are losing effectiveness, and shareholder returns are increasingly disconnected from broader market performance.

This situation is not cyclical. It reflects a misalignment between how value is created in CPG today and how markets and consumers now reward value creation.

Over the last several years, even the best-performing CPG companies have delivered meaningfully lower returns than broader equity markets, a signal that scale, brands, and industrial excellence, while still essential, are no longer sufficient on their own to support long-term value creation.

In recent years, much of CPG growth has been sustained through pricing. This strategy has bought time, but not a solution to the underlying problem that has been simmering for a while.

Private labels, insurgent brands and local players continue to gain share across markets while an increasing number of consumers trade down or fragment their spend across brands, channels, and solutions. At the same time, promotional intensity and marketing efficiency have deteriorated, further eroding the effectiveness of traditional levers.

The implication is clear: price can no longer compensate for weak demand fundamentals.

In 2025 for the top 11 CPG companies volume growth has been negative. In 2024, roughly three-quarters of consumer products sales growth came from price increases.

Over the past 5 years, consumer staples (proxied by XLP) delivered ~8.0% annualized CAGR vs. ~15.0% annualized for the S&P 500 (SPY). In 2025 the top 11 CPG companies’ share price growth was on average at 0% vs. double digit growth of the relative stock exchange indexes.

This creates a new mandate: CPG must reinvent the consumer value equation, while still extracting medium-term value through disciplined penetration-driven volume growth.g analysis should be read.

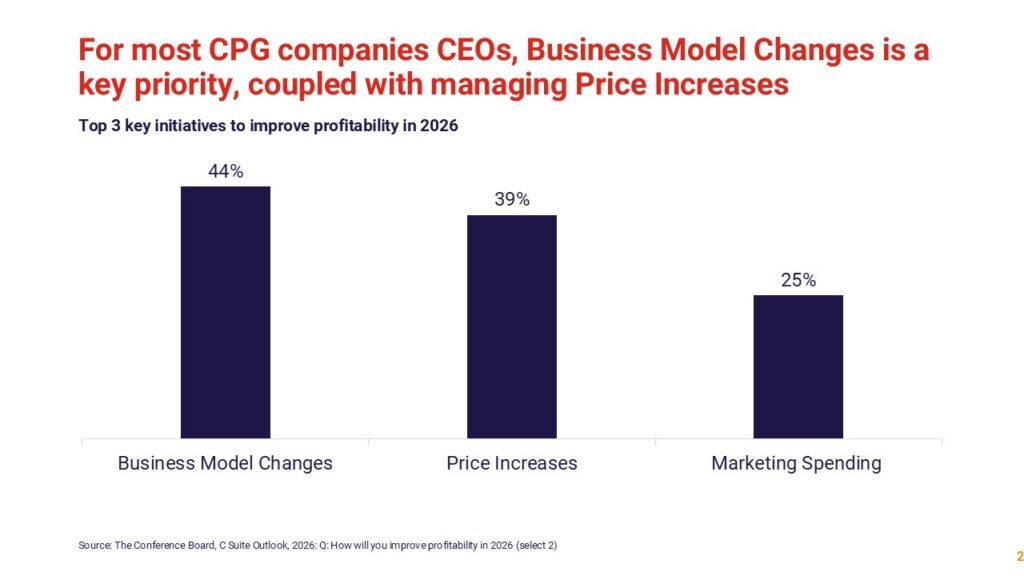

CEOs recognize the need for a reset

This reality is now reflected at the highest level of corporate priorities. Recent global CEO surveys show that business model change ranks as the number one priority, ahead of price increases, marketing spend, headcount optimization, or M&A.

Price increases remain high on the agenda, but they are increasingly being viewed as tactical levers, not sustainable engines of value creation.

Similarly, an excessive focus on the premium categories or segments is leading to two consequences for global CPG players:

- Inevitable excess capacity in production plants as a lower number of consumers are being focused on, those who can afford to pay more

- Leaving the bulk of category volumes in the hands of regional/local players in the mid tier price segments

- Allowing smaller brands and private labels to first control the lower price segment and then start to ladder up.

For CPG in particular, this shift is significant. The industrial model that historically underpinned competitive advantage, capital-intensive assets, scale manufacturing, and fixed-cost leverage, is now acting, in many cases, as a constraint on adaptability.

Why industrial scale alone no longer drives CPG value creation

Manufacturing scale, operational excellence, and industrial know-how will remain critical components of any successful CPG model. However, they can no longer sit in isolation at the center of the value equation.

Three structural tensions are emerging:

- Capital intensity limits experimentation and speed

- Traditional category boundaries constrain innovation and relevance

- Indirect routes to market reduce access to consumer insight and learning velocity.

As a result, optimizing the existing system delivers diminishing returns. Yet this does not mean CPG companies are “out of growth.”

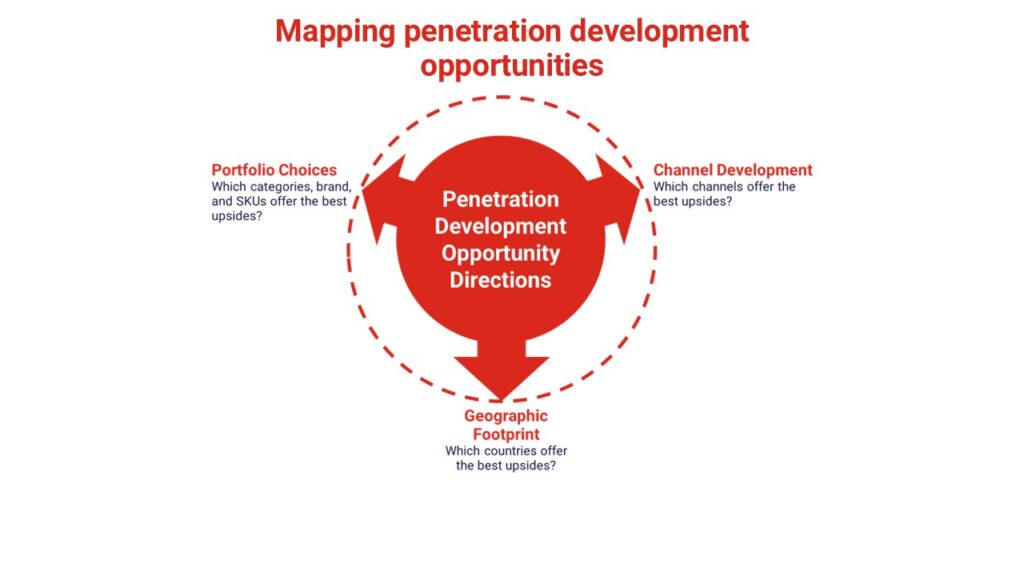

The medium-term opportunity: penetration-led volume growth

In the medium term, large CPG companies can still sustain value creation through volume growth, but the nature of that growth is changing. The most credible path forward is penetration-led volume growth, not indiscriminate expansion. This requires deliberate choices involving three dimensions:

Portfolio choices become critical.

Growth increasingly depends on focusing portfolios on consumer jobs to be done and occasions where penetration headroom still exists, on adjacent or redefined spaces where brands have permission to stretch, and on managing explicitly the difference between cash engines and growth engines, each with distinct roles, economics, and expectations.

Channel development is equally decisive.

Penetration today depends on structural advantage in the channels that are gaining relevance like discounters, e-commerce, quick commerce, specialized platforms, Away From Home and digital B2B ecosystems. As pointed out by Justing Sargent in our recently published article “The Collaboration Dividend” growth can come also from existing channels.

Geographic footprint must also be addressed more selectively. Growth is increasingly uneven across markets, requiring targeted geographic bets, localized propositions, and tailored pack-price and route-to-market architecture rather than uniform global rollouts.

Penetration-led growth, therefore, is not primarily an execution challenge. It is a design problem, requiring a different way of thinking about where and how growth is created.

Disruptive innovation as the bridge between growth and new business models

This is where disruptive innovation becomes essential, provided it is understood in a broader and more holistic sense than traditional product innovation and it is fully consumer centric.

At its core, penetration-led growth must be built around a consumer-first engine structured on three elements:

- Jobs & occasions (demand definition)

- Access & interfaces (demand access)

- Portfolio & economics (value capture).

Disruptive innovation, therefore, is not just about new products, but about designing and activating this system end-to-end.

In CPG, innovation has long been associated mainly with new products, formulations, or line extensions. While these remain important, they are no longer sufficient to unlock sustainable penetration growth or to support the emergence of new business models.

Disruptive innovation today operates at the system level. It reshapes how value is conceived, created, delivered, and captured, often without immediately challenging the core product itself. In doing so, it allows companies to explore new growth logics while continuing to leverage existing industrial and brand assets.

In practice, this broader form of innovation spans multiple, interconnected dimensions:

- Consumer innovation, redefining the consumer job to be done and reframing categories around outcomes, occasions, and routines rather than products

- Business model innovation, experimenting with new revenue logics, subscription mechanisms, service layers, and ecosystem participation

- Route-to-market innovation, redesigning channels, partnerships, and digital interfaces to accelerate reach, learning, and penetration

- Operational and capability innovation, embedding data, AI, and automation to increase adaptability and decision speed

- Organizational and governance innovation, enabling faster experimentation, cross-functional collaboration, and different risk profiles.

Crucially, this systemic view of innovation is what makes penetration-led growth sustainable.

By redefining occasions, simplifying access, improving relevance, or lowering adoption barriers, disruptive innovation expands demand rather than merely increasing intensity among existing buyers.

At the same time, it creates protected spaces where new ways of generating value can be developed and tested without destabilizing the core business.

Clearly some of these routes are harder than others and overall ROI can be different.

To manage disruptive innovation properly aligning the right resources and capabilities becomes crucial as well outlined by our Partner Mauro Piloni in his recent article “Unlocking Growth in the CPG Industry in a World of Uncertainty”.

Why business model innovation becomes unavoidable

Even with disciplined penetration-led growth, the limits of the traditional CPG model remain. This is why leading players are exploring new business models, not as experiments at the margin, but as ways to redefine how value is created.

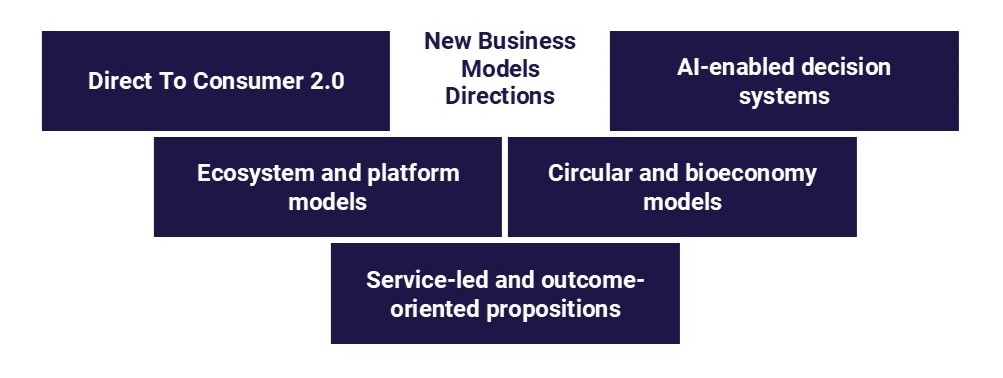

Across the industry, five model directions are emerging:

- Direct-to-Consumer (DTC) 2.0, not as a volume channel but as a strategic control tower for data, insight, and innovation and to reduce dependency from large retailers.

- Ecosystem and platform models, where value is created across connected products, services, and partners. Think here at how wearables have been able to build a market as a health and data companion.

- Service-led and outcome-oriented propositions, shifting from selling items to delivering results and covering higher level consumer needs. This provides more rounded solutions to consumers.

- Circular and bioeconomy models, where sustainability becomes a core operating logic driven by regulation and economics. I.e. in many markets, refill models already exist at scale, for example, returnable glass bottle systems, and could be reinvented through electrified logistics and digital tracking.

- AI-enabled decision systems, i.e. across dynamic pricing, demand sensing and portfolio optimization.

These models rebalance the mix between tangible assets and intangible value, between scale and adaptability.

These five models are not alternatives. They are different expressions of three underlying transformation pillars being:

- Demand definition – How can I tackle new, or better addressing existing, jobs to be done and occasions through a mix of physical products and services?

- Demand access – How can I reinvent route-to-market leveraging new interfaces?

- Operating adaptability – How can I better leverage data and AI pairing it with new organization models?

The real challenge: transitioning without breaking the base

While CEO ambition to redefine business models is clear, the path to get there remains uncertain. Capital investment and industrial footprint, once the primary drivers of value, now act as potential barriers to transformation.

The challenge is not to abandon the existing model, but to transition from it deliberately, funding the future while protecting the present.

This requires:

- Clear transition architectures, not isolated pilots

- New performance metrics beyond volume, margin, and share

- Explicit trade-offs between short-term optimization and long-term optionality

Across all emerging models, three enablers consistently determine success:

- Access to fresh, clean, harmonized internal and external information

- Experience-based, multidisciplinary, future-oriented human judgment

- A seamless combination of the two, where technology amplifies, not replaces, human insight

This is where many transformations fail: not for lack of data or technology, but for lack of meaningful synthesis and direction.

The Sevendots perspective

At Sevendots, we have been consistently advocating for some time that the CPG value equation must evolve, both to secure long-term shareholder returns and to better align with consumers’ rapidly evolving expectations. Not only have we been beating this drum, but we have been working with multiple companies to kick start and manage the required change.

What differentiates our work is not the identification of growth opportunities, but the ability to sequence penetration-led growth and business model evolution without breaking the industrial base.

More recently, we have been promoting our strong belief that large CPG companies can still grow volumes in the medium term, provided growth is driven by penetration rather than short-term intensity.

Supporting this, we have developed a clear and pragmatic penetration-growth framework that helps companies identify where real demand headroom still exists and how to unlock it through the right combination of portfolio choices, channel design, and geographic focus.

In practice, we work with leadership teams to:

- Identify penetration opportunities across consumer jobs, occasions, and adjacent need states

- Redesign portfolios to clearly differentiate between cash engines and growth engines

- Translate strategic intent into concrete channel and route-to-market choices that accelerate reach and learning

- Prioritize geographies where penetration-led growth is structurally achievable rather than assumed.

Beyond penetration, we are actively working with and alongside clients on the broader set of transformations required to redefine value creation in CPG. This includes sharing experience, co-designing solutions, and supporting execution across topics such as:

- Moving beyond traditional category definitions toward consumer- and solution-led growth spaces

- Rebalancing tangible and intangible elements of the value proposition

- Designing higher-level consumer solutions that aggregate products, services, and data

- Rethinking routes-to-market, including DTC, digital B2B, and ecosystem-based models

- Exploring open and collaborative ecosystems where cross-company partnerships improve efficiency and quality of the offer

- Leveraging disruptive innovation and AI-enabled capabilities to accelerate insight, adaptability, and decision-making.

Across these engagements, our focus is not on isolated pilots, but on helping organizations manage the transition from today’s industrial model towards more adaptive, insight-driven business models while protecting the economic engine that funds the journey.

Closing thought

In 2026, the question for CPG leaders is no longer whether they can protect margins in the short term.

It is whether they can reconcile penetration-led volume growth with a fundamental redefinition of how value is created.

Business model evolution is no longer optional. It is the condition for sustainable growth and long-term shareholder returns

For CPG leaders, the real risk is no longer disruption from the outside but clinging too long to a value equation that markets and consumers have already moved beyond.