Business Strategy 10 April 2026

2025: A Structural Divide in Global CPG performance

Volume has turned structural, not cyclical, and it directly impacts companies’ ability to sustain value creation.

The year marks the end of price-led complacency and companies must rapidly evolve to adapt.

Sevendots, Rome

7 minute read

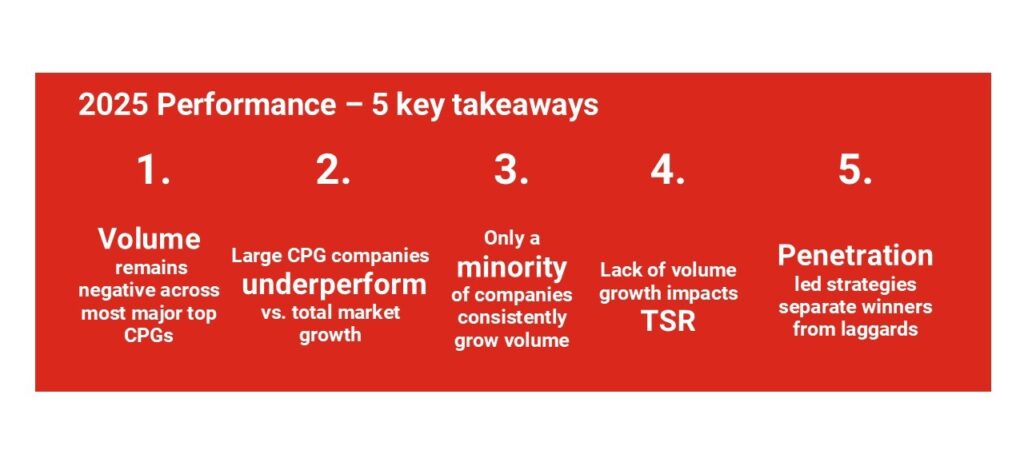

5 key takeaways from 2025 performance

2025 has marked a systemic inflection point for large global CPG companies.

The narrative is no longer about inflation, temporary elasticity, or tactical adjustments. The data shows a widening divide in volume, in scale, and increasingly in financial performance.

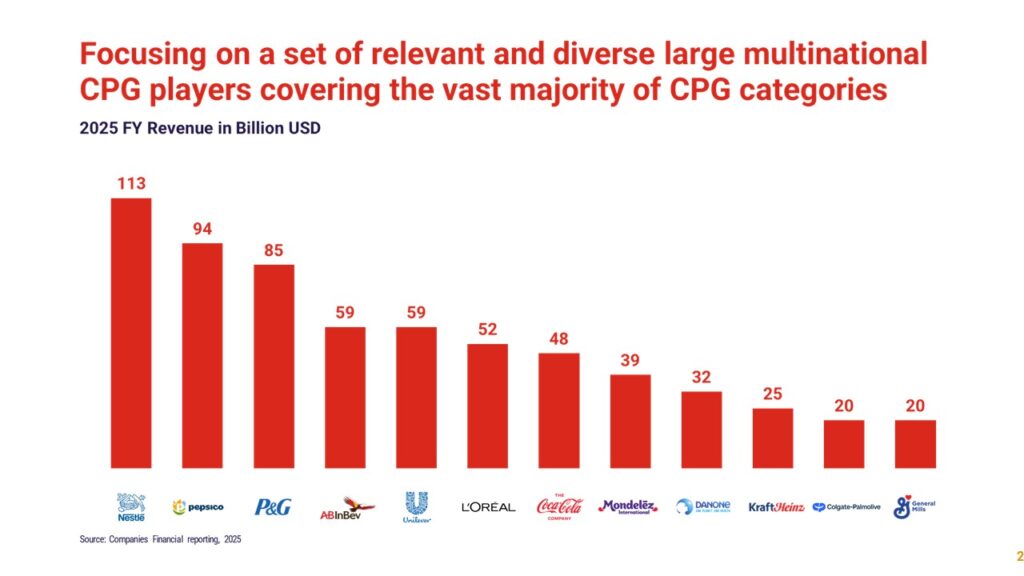

Based on our review of 12 among the top global CPG players, five key takeaways stand out.

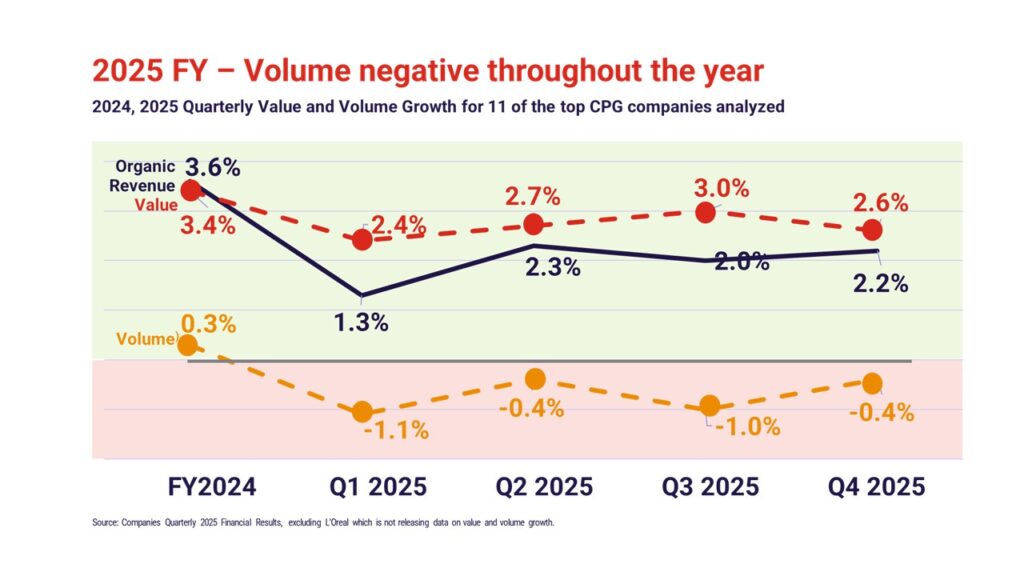

1. Volume remains negative across major CPG companies

Unlike 2024, when volume growth was modest but still positive (+0.3%), 2025 shows a negative volume trend across all four quarters.

As we already highlighted in our analysis of the Q2 2025 CPG Results, early signs of structural volume pressure were already visible.

It’s now even clearer that this is no longer cyclical softness. It is persistent.

Several forces are converging:

- Shifting consumer behavior and higher price elasticity

- Geopolitical instability and tariffs variability

- Commodity cost inflation

- Retail destocking in selected markets

- Limited disruptive innovation

Pricing has supported topline growth in recent years. But pricing alone does not expand physical scale. And in 2025, volume weakness became visible across most large players.

2. Large CPG companies underperform the market

The overall CPG market grew faster than the large multinational players analyzed.

The growth gap: 1.3 percentage points.

More importantly, the difference is primarily volume-driven.

While market volume remained positive, large CPG players on average experienced negative volume growth, building a 1.5 pp gap.

When leaders grow below market, scale erodes. And when scale erodes, share shifts.

Where is growth going?

- Private Labels, growing above the market across regions and strongest where historically underdeveloped

- Insurgent brands, faster overall (particularly in innovation) and more aligned with emerging consumer trends

- Local players, leveraging proximity, agility, and cultural relevance

Private Labels, in particular, follows a consistent path across regions. Europe represents the most advanced stage, with some markets exceeding 50% share, a potential preview of a longterm evolution elsewhere.

The competitive set has fundamentally changed.

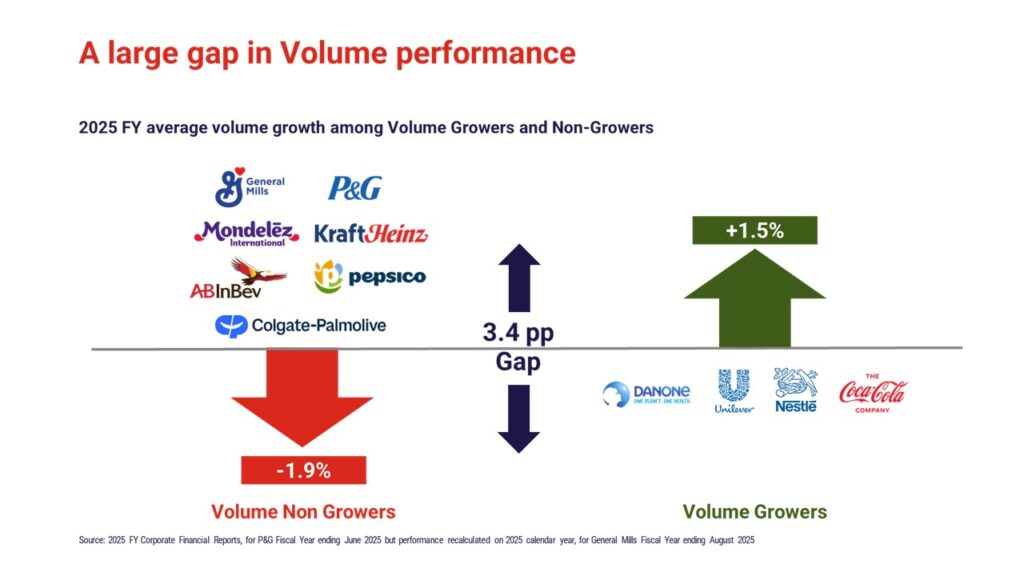

3. Only a minority of global CPG leaders consistently grow

volume

Out of the top CPG players analyzed, only four delivered volume growth in 2025.

The performance gap is striking, with a 3.4 pp divide between volume growers and volume non-growers.

Even more telling: the companies that grew volume in 2025 were largely the same that grew in 2024 (with only one exception). This suggests that volume growth is not random. It reflects structural choices.

- Clear portfolio prioritization.

- Geographic discipline.

- Channel expansion.

- Execution rigor.

Volume is becoming a discriminator of strategic coherence.

4. Lack of volume growth impacts margin and TSR

There is a growing volume-margin tension.

In 2024, companies were able to expand margins despite limited volume growth. Pricing and productivity offset weak physical expansion. In 2025, average negative volume growth had a negative impact on margins.

Without scale, operating leverage weakens.

The impact extends to capital markets.

Average share price performance across major players in 2025 was 0%.

But within that average:

- Volume growers: +8%

- Flat or negative volume players: –8%

Markets reward physical growth. Not pricing-led revenue.

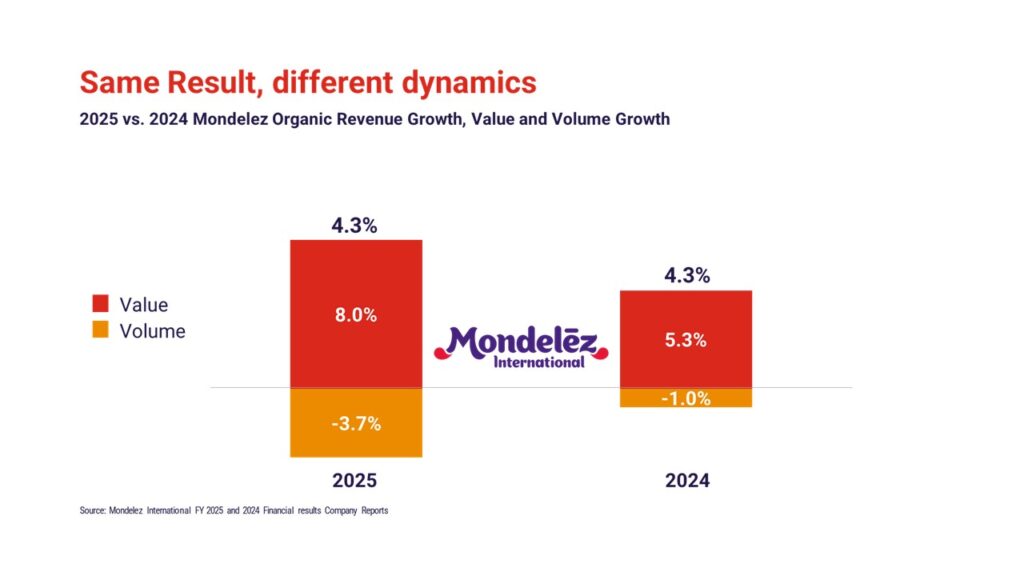

The case of Mondelez illustrates the tension. Organic growth remained stable year-over-year (4.3% in both 2024 and 2025), but the mix shifted dramatically, greater volume loss offset by stronger pricing. At the same time, margins declined significantly Gross margin declined by almost 600 bps and operating margin by 300 bps, partly driven by cocoa inflation.

Volume and value are not independent.

Persistent volume erosion can create a vicious cycle.

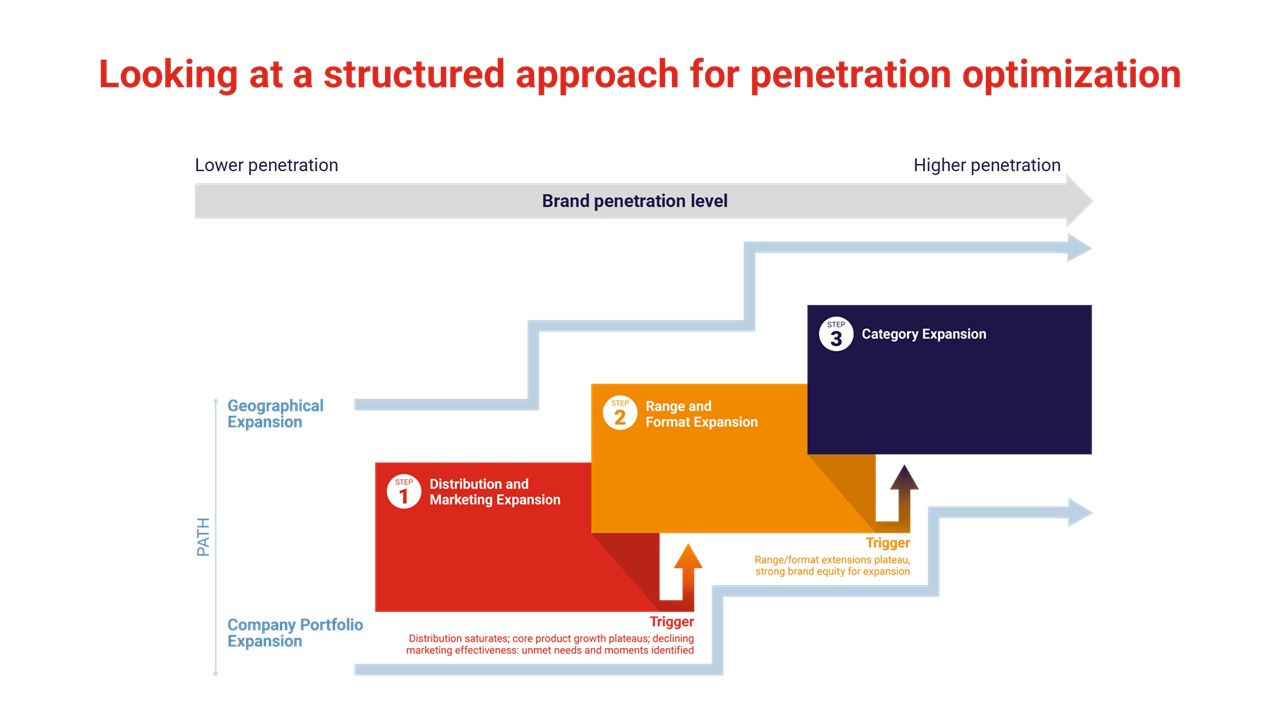

5. Penetration-led strategies separate winners from laggards

If volume is the problem, penetration is the solution.

The correlation between volume and penetration is significantly stronger than between volume and frequency. This structural relationship is explored further in our Penetration Analysis Growth Series. Yet penetration remains underleveraged across many large CPG portfolios.

The average global household penetration of the top 50 brands is just above 20%. The upside remains substantial.

Few multinational players have more than a handful of brands in the global top 50. Unilever stands out with 12; a few have four or six brands, most others have only one or two.

Driving penetration requires disciplined choices:

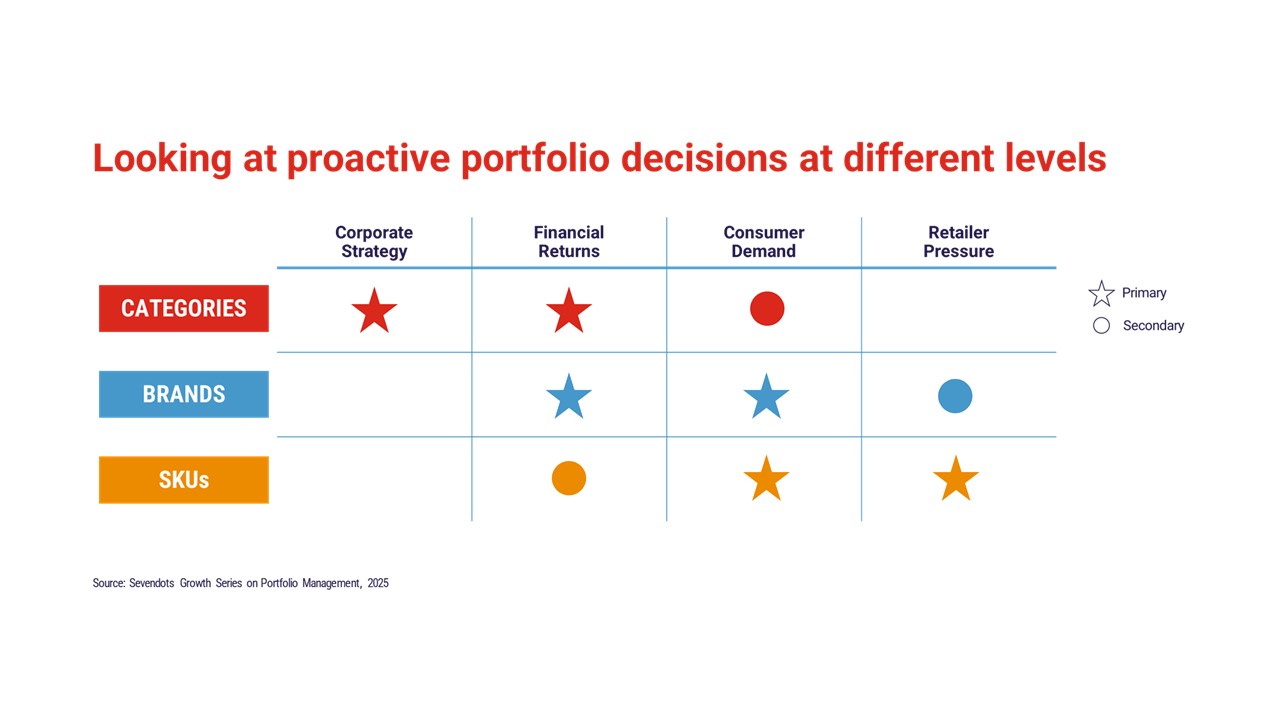

Portfolio

Systematic review at category, brand, and SKU level.

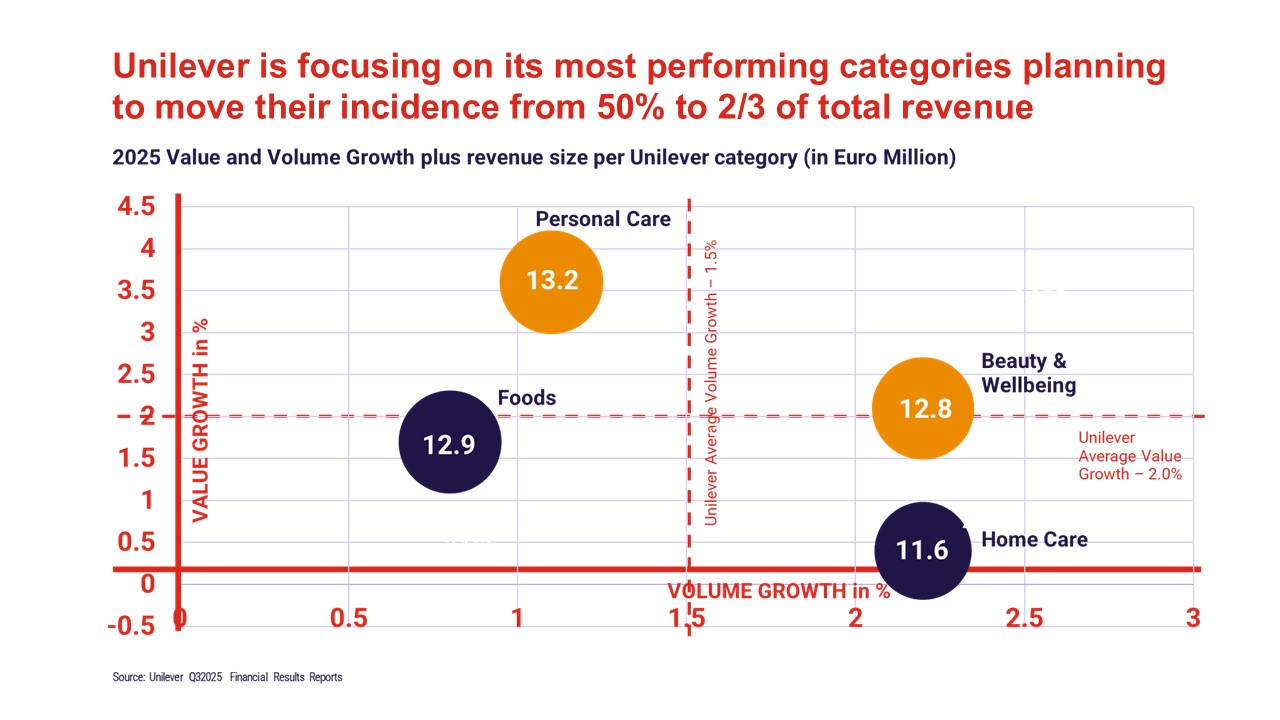

Unilever provides a clear example, sharpening its focus on Beauty & Wellbeing and Personal Care, which today represent 51% of revenue and are planned to grow to two-thirds of the portfolio, divesting structurally declining segments, and explicitly adopting a volume-led execution model.

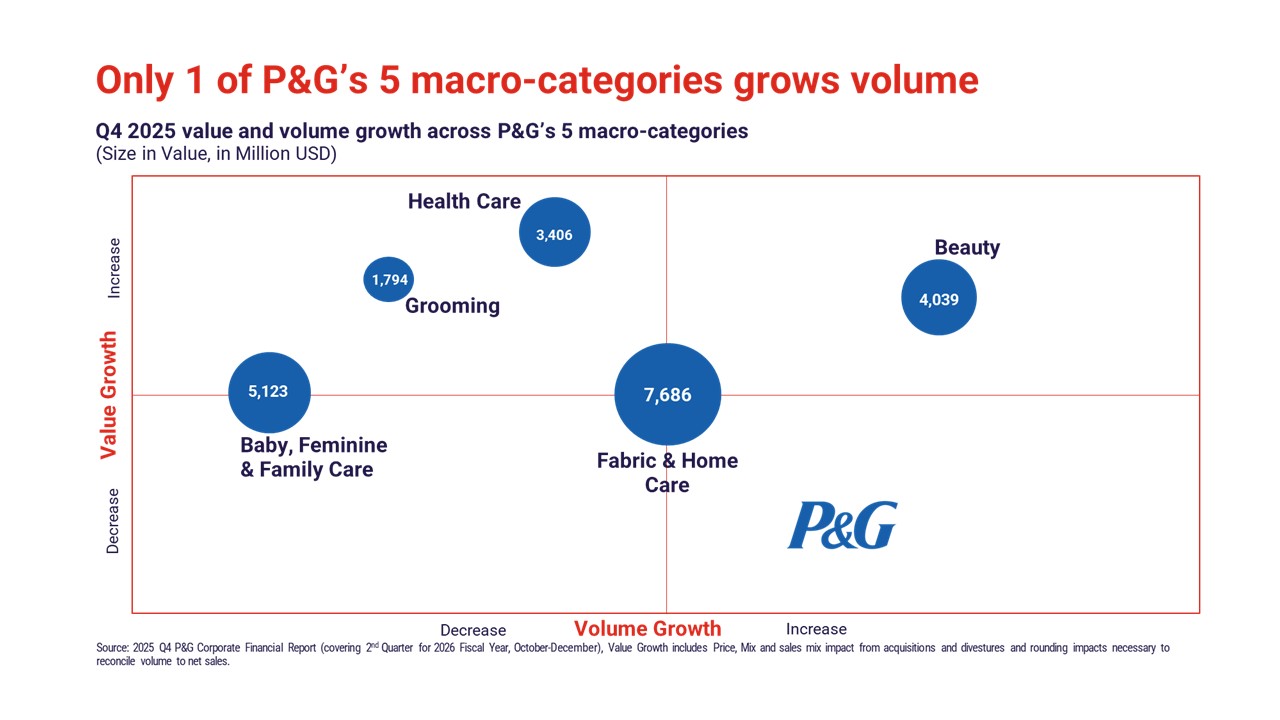

P&G’s 2025 volume challenges, with only one macro-category growing, reinforce the need for portfolio reassessment.

Portfolio assessment should be periodic and holistic.

In many organizations, reviews are driven either by centralized financial metrics or by BU-level consumer and market insights. Sustainable growth requires combining both, integrating financial performance, consumer demand, competitive and retailer dynamics, alongside broader external factors such as regulation, sourcing risk, and geopolitical volatility.

The Sevendots framework links portfolio decisions at category, brand, and SKU level to these integrated triggers, supporting more disciplined and strategic allocation choices.

Channels

Channel fragmentation is accelerating.

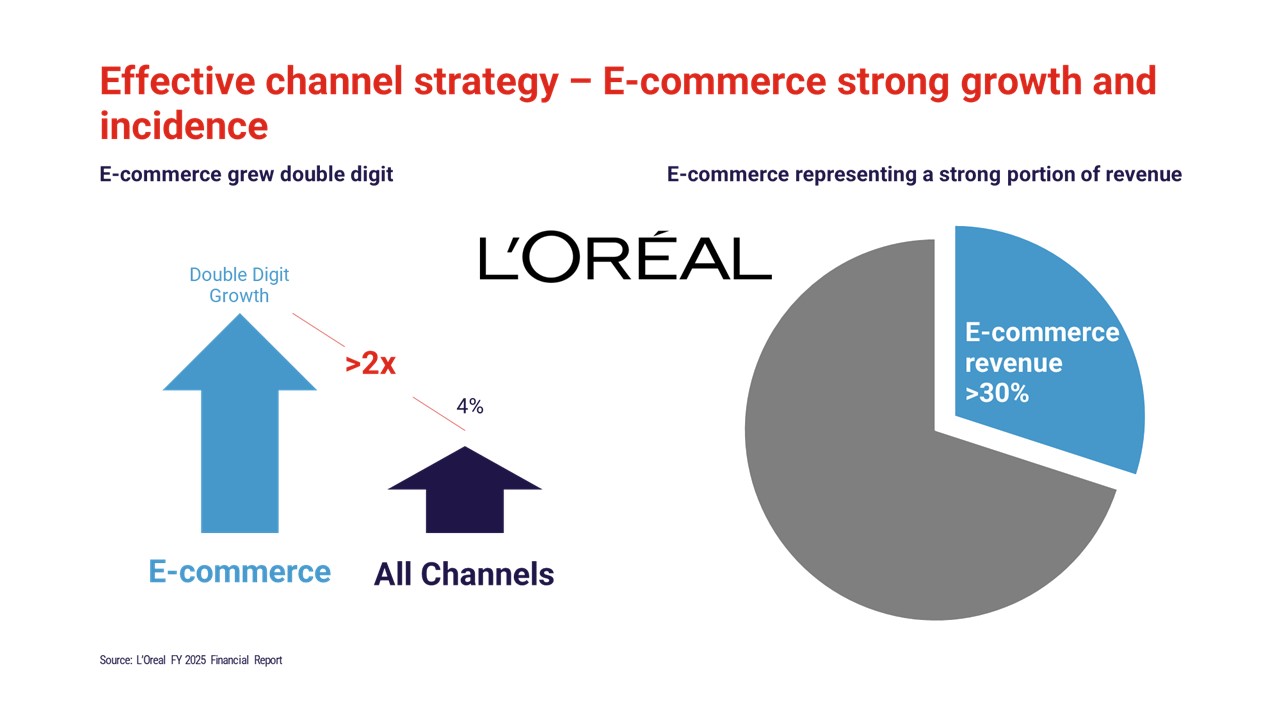

L’Oréal and Nestlé demonstrate strong momentum in e-commerce; Nestlé and others also leverage Away-From-Home. Danone reports faster growth outside mass retail.

Expanding distribution reach and strengthening execution across channels directly fuels penetration.

“In 2025, channels outside mass retail grew significantly faster than mass retail. We are reaching more people in more places at all stages of their lives.”

Danone

Geography

Geographic expansion remains underexploited.

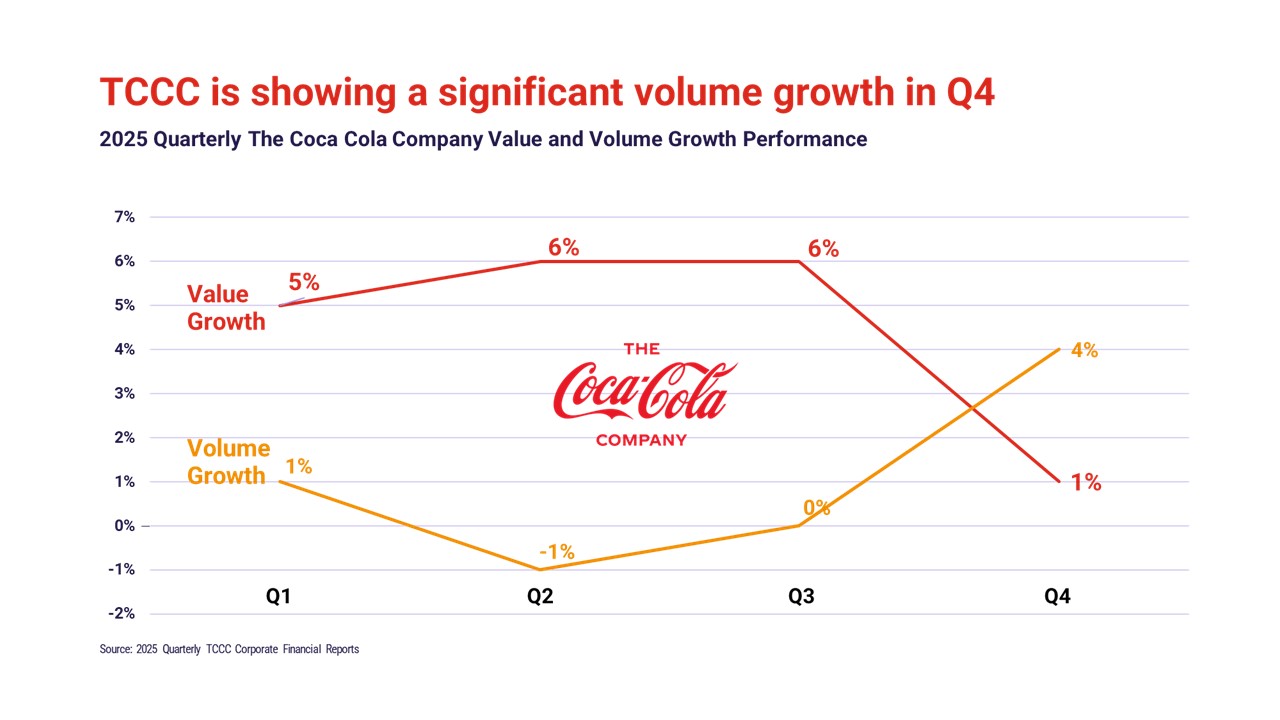

The Coca-Cola Company Q4 2025 pivot, with volume accelerating ahead of value, reflects renewed focus on emerging markets where many beverage occasions remain unbranded.

“More from more markets” is not just rhetoric, it is a penetration strategy.

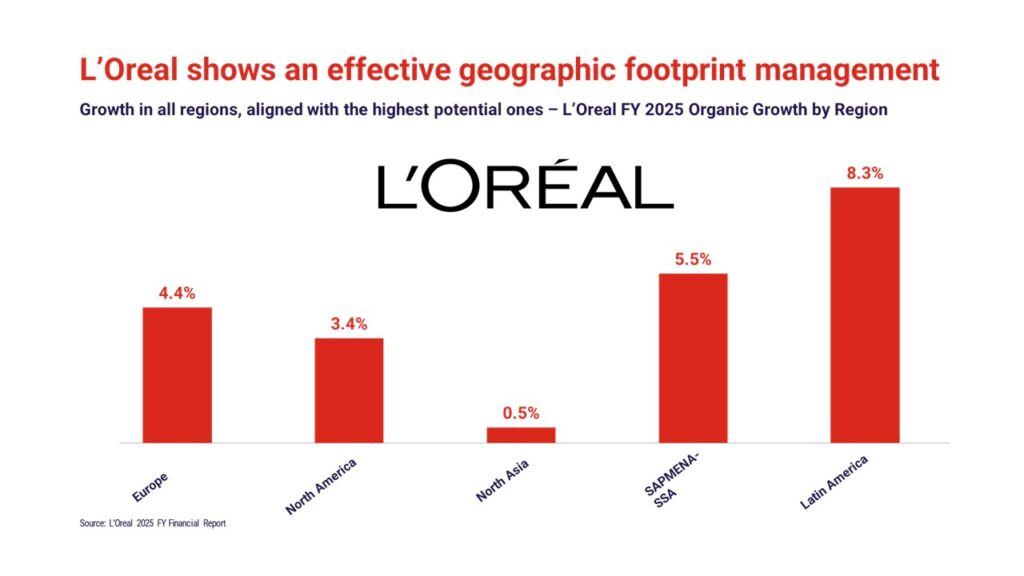

L’Oréal illustrates disciplined geographic alignment. In 2025, the company grew across all regions, with particularly strong performance in Latin America and SAPMENA-SSA, two of the most dynamic global CPG regions. By aligning its footprint with higher-growth markets, L’Oréal benefits directly from regional momentum, reinforcing geography as a foundational driver of penetration and scale.

Geographic prioritization should not be limited to evaluating the current size of a category in a market — a conservative approach often seen in large organizations. The real opportunity lies in identifying where a company can build category leadership and capture disproportionate growth. Expansion decisions should therefore be linked to the potential to shape demand, drive penetration, and establish a defensible position — not merely to participate in existing scale.

Innovation

True innovation remains underleveraged. As discussed in our Consumer-Facing Innovation Growth Series, structured innovation discipline is directly linked to long-term shareholder return. Global new product intensity has declined. Yet companies that focus on structured, disciplined innovation consistently outperform in shareholder return.

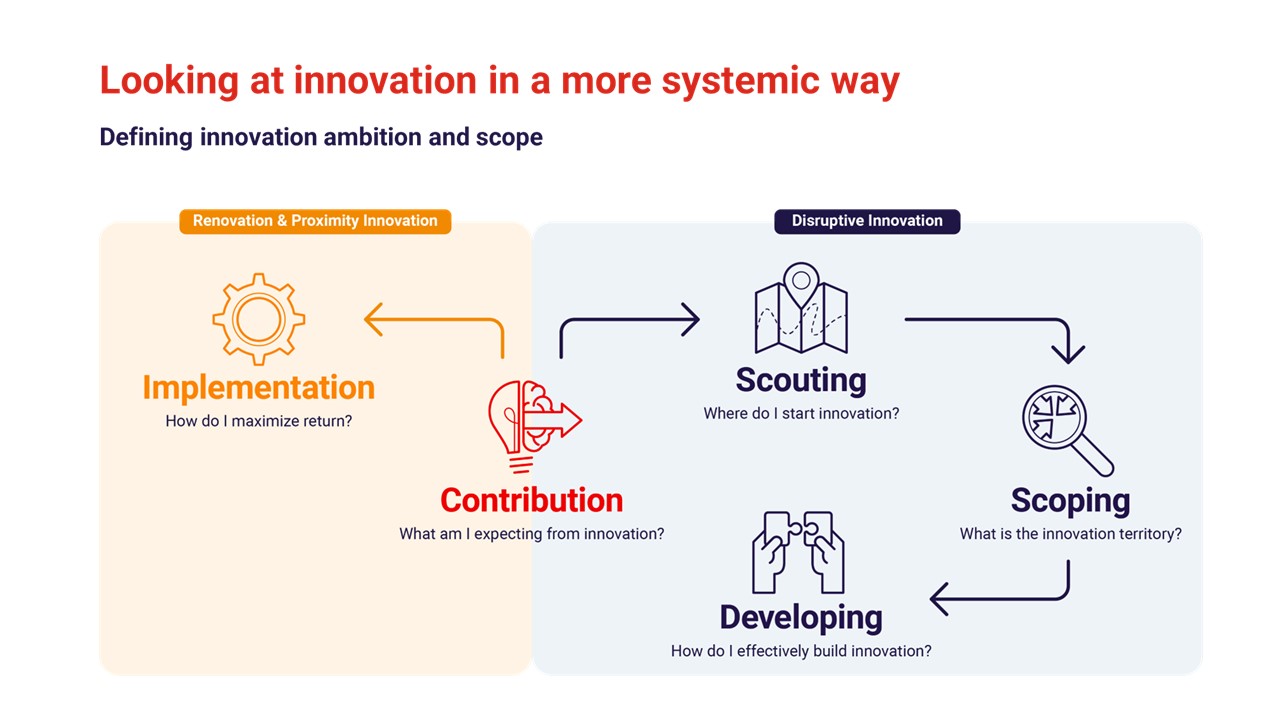

Innovation must be differentiated between renovation and real disruptive expansion.

Innovation requires clarity. It should begin with a clear definition of its expected contribution and then follow differentiated paths. Renovation and proximity innovation aim to optimize and reinforce existing assets, while disruptive innovation demands dedicated scouting, scoping, and development logic. Treating these streams distinctly enables more disciplined resource allocation and more consistent long-term impact.

Strategic imperatives for 2026

The lessons from 2025 are clear:

- Rebalance from price-led to volume-led growth

- Elevate penetration to a board-level KPI

- Prune portfolios aggressively

- Double down on high-growth geographies

- Expand distribution reach and strengthen execution across channels

- Make innovation selective and transformational

2025 did not simply expose temporary weakness but it revealed a structural divide where volume now discriminates winners from laggards.

The performance indicates that scale underpins margins and that physical growth drives valuation. For large CPG leaders, the question is no longer whether volume matters, but whether strategy is aligned to deliver it.

How Sevendots supports penetration-led growth

Translating these imperatives into execution requires structure and discipline.

At Sevendots, we work with leadership teams to design and implement penetration-led growth strategies grounded in data and strategic clarity. Our work spans large multinational CPG leaders and medium players across categories and geographies.

Our framework for penetration planning and optimization allows companies to:

- Map and assess current assets across categories, brands, and SKUs

- Conduct deep portfolio diagnostics combining financial performance, consumer dynamics, and external market variables

- Identify where penetration potential is structurally underleveraged

- Define clear choices on where to focus, expand, simplify, or exit

- Align channel and geographic expansion with portfolio priorities

- Redefine innovation ambition and ensure resources are allocated to initiatives that expand scale, not just sustain mix.

Penetration does not increase by chance.