Business Strategy, Portfolio Management 28 June 2026

The Return of Volume: Why the Largest CPG Companies Are Changing Their Growth Playbook

After years of chasing pricing, the world's largest CPG companies are rediscovering volume.

Q1 2026 may mark the beginning of a fundamental shift in how growth is created.

The winners are making deliberate choices around portfolio, geography and penetration, not simply lowering prices.

The question is no longer whether volume matters, but how to build it sustainably.

Sevendots, Rome

8 minute read

The beginning of a strategic reset

For the first time in almost two years, something meaningful is happening in the CPG industry.

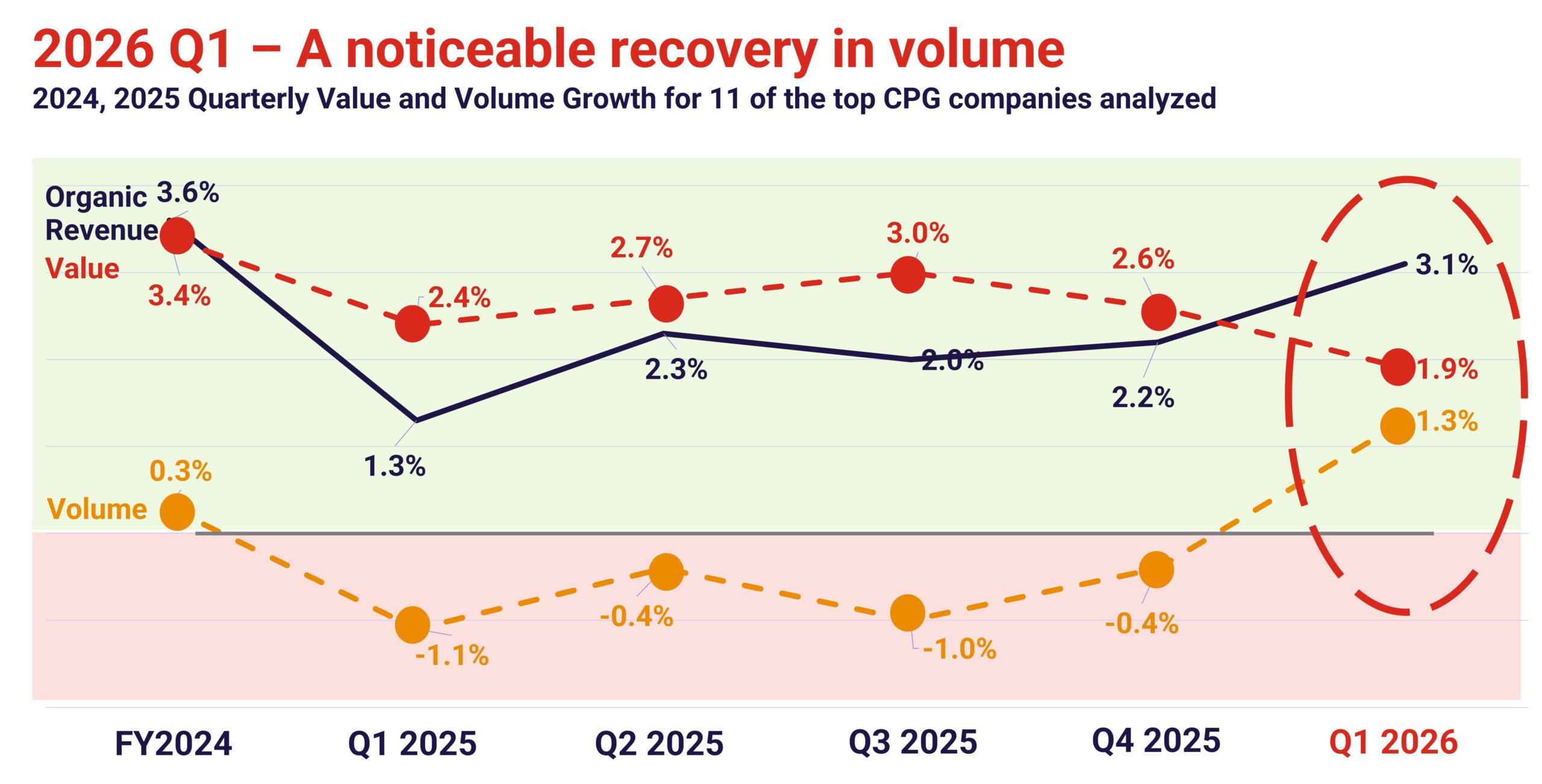

After a relatively flat 2024 and four consecutive quarters of declining volume throughout 2025, the largest global CPG companies are finally showing a noticeable recovery. Across the eleven companies analyzed (excluding L’Oréal, which does not disclose volume data), average volume growth exceeded 1% in Q1 2026 while average organic growth remained at a healthy 3.1%, suggesting that companies are beginning to replace pricing-driven growth with healthier, volume-led expansion.

On the surface, this may look like simply a stronger quarter. In reality, it could represent the beginning of a much deeper strategic shift.

More importantly, it may signal that the industry’s largest players have finally acknowledged a fundamental truth: pricing alone cannot sustain long-term growth, whether this shift is internally driven or triggered by financial market pressures.

Inflation changed the industry’s definition of growth

The inflationary years fundamentally reshaped how many CPG companies approached growth.

Between 2022 and 2025, pricing became an extraordinarily powerful lever. Companies successfully offset unprecedented increases in raw materials, logistics and labor costs by implementing multiple rounds of price increases, often delivering record organic growth while protecting margins.

Financially, the strategy worked. Culturally, however, it also changed the way many organizations thought about success. Revenue growth has increasingly become the headline KPI. Value market share became the preferred measure of commercial progress. Quarterly discussions naturally focused on pricing execution, revenue management and margin protection. Meanwhile, two of the industry’s most fundamental measures, volume and penetration, gradually lost strategic prominence.

Inflation, in many respects, gave the industry the illusion of almost unlimited top-line growth through pricing. That illusion lasted until consumer behavior began to change. As affordability deteriorated and household budgets tightened, consumers became increasingly price sensitive. Purchase frequency declined across multiple categories. Consumers traded down to private labels, smaller local brands and alternative channels. In many cases they simply eliminated purchasing occasions altogether.

The consequences became increasingly visible during 2025, when most of the large multinational experienced persistent volume declines despite still reporting positive revenue growth. The industry’s growth engine had become increasingly dependent on pricing while its underlying consumer base was slowly weakening.

Q1 2026 suggests companies have recognized the problem

The most encouraging aspect of Q1 is not the return of volume itself but it is the number of companies now actively pursuing it.

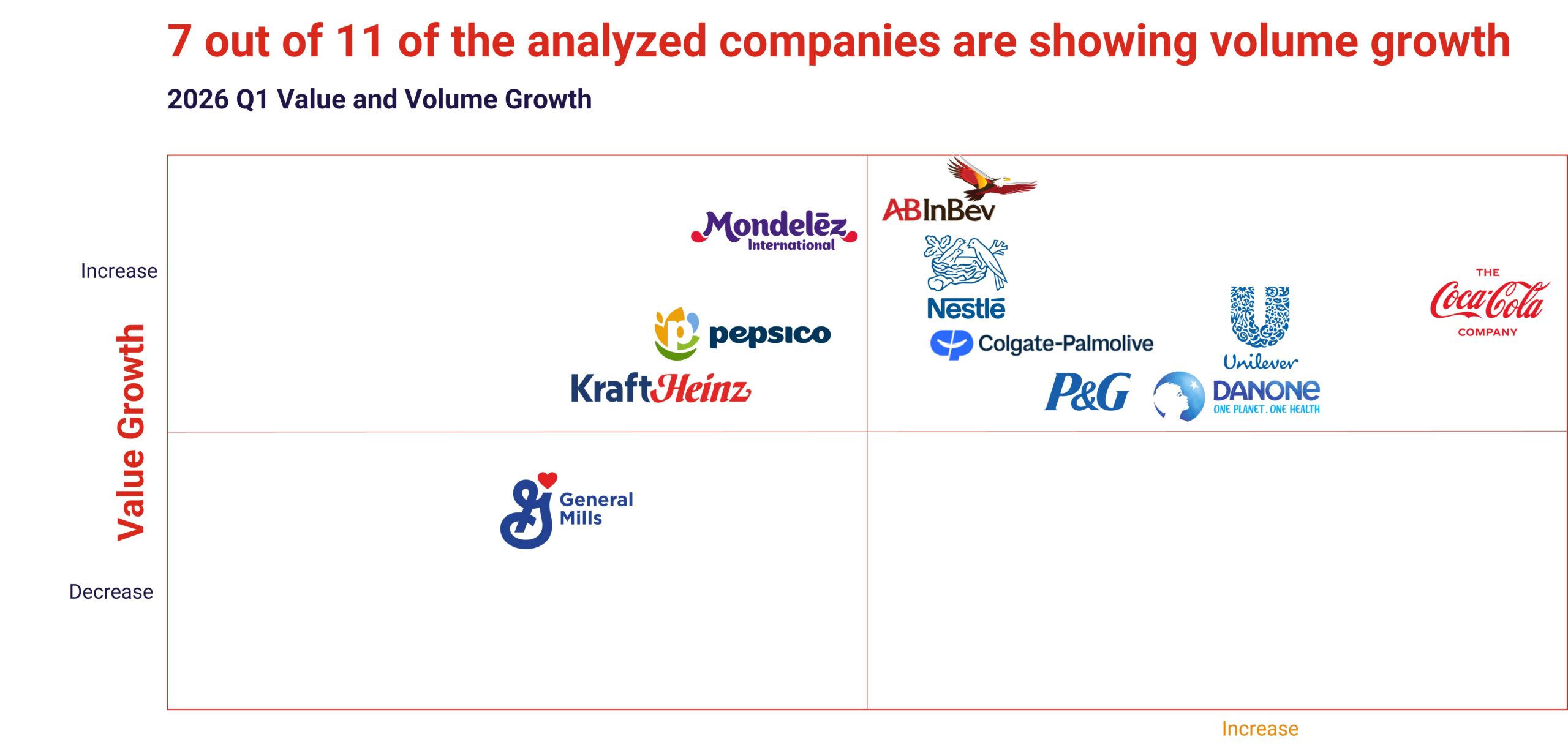

Only a year ago, just four of the largest CPG companies consistently reported positive volume performance. In Q1 2026, eight out of the twelve companies analyzed delivered positive volume growth, with AB InBev, P&G and Colgate-Palmolive joining companies such as The Coca-Cola Company, Unilever, Danone and Nestlé.

This reflects an industry gradually rediscovering that volume is not simply another KPI but it is the physical manifestation of penetration. Every additional unit sold represents another purchasing act, another household recruited, another consumption occasion captured, another opportunity to reinforce brand relevance.

Ultimately, volume remains the strongest indicator that a company is genuinely expanding its consumer franchise rather than simply extracting more value from existing buyers.

Volume cannot be promoted into existence

One of the recurring lessons emerging from the Q1 results is that companies are not growing volume through promotions alone but they are making deliberate strategic choices.

Three themes consistently emerge.

First, portfolio focus.

Successful companies are becoming increasingly selective about the categories, brands and pack formats they invest behind.

Rather than attempting to maximise breadth, they are concentrating resources where consumer demand, differentiation and scalability are strongest.

Second, geographic prioritization.

Growth is increasingly concentrated in markets where demographics, affordability and category development remain favourable. Rather than treating every geography equally, leading companies are allocating disproportionate investment behind higher-potential regions.

Third, cultural relevance.

Brands that create stronger emotional connections with consumers increasingly generate more purchasing occasions, improving both penetration and consumption frequency.

Perhaps no company illustrates this better than The Coca-Cola Company.

Coca-Cola shows what the new growth playbook looks like

Among all companies analyzed, Coca-Cola provides perhaps the clearest evidence of how the industry’s growth model is evolving.

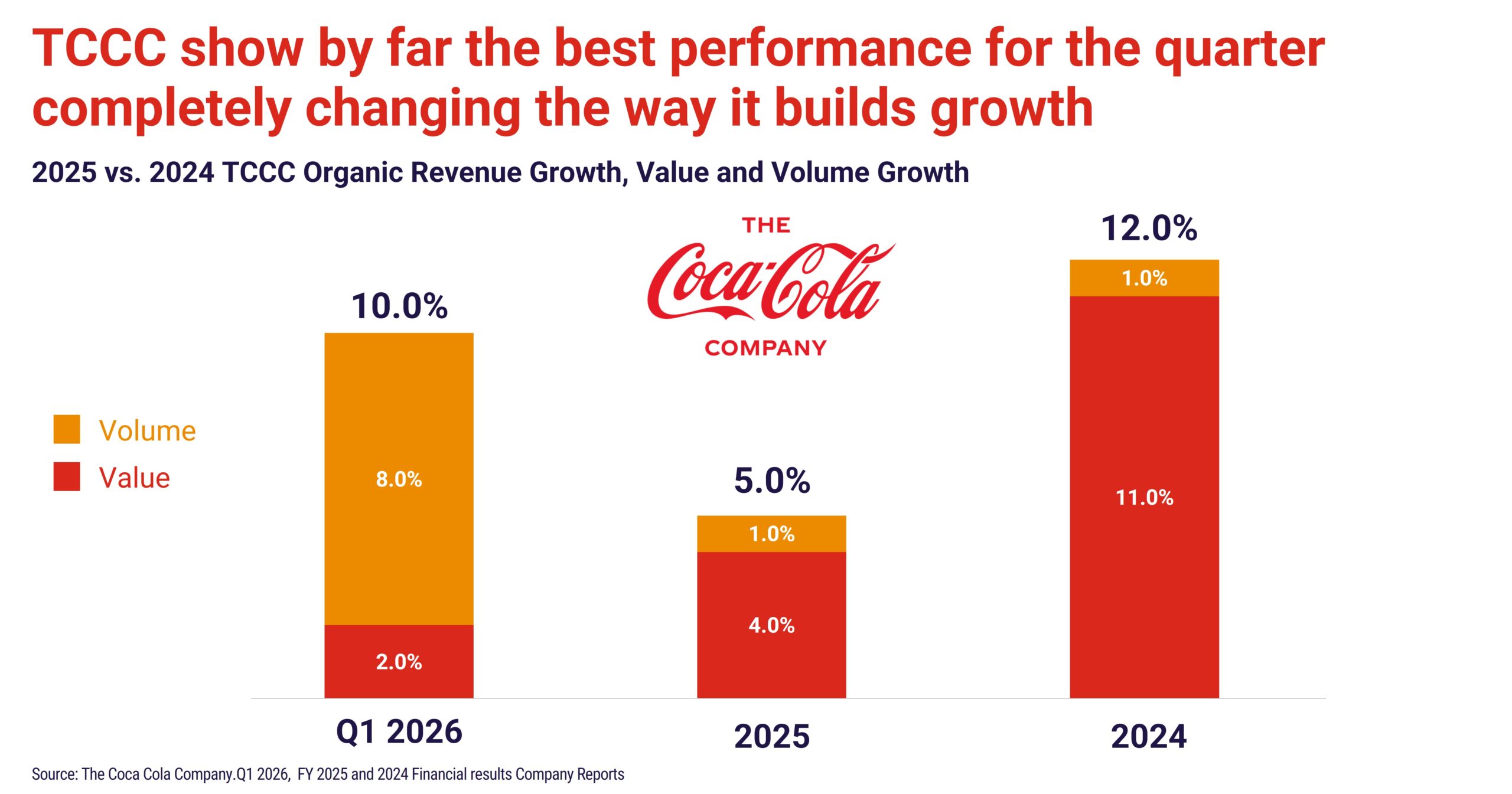

Only two years ago the company represented one of the strongest examples of pricing-led expansion. Its extensive portfolio rationalization and disciplined revenue growth management significantly improved price-per-liter across the business, allowing Coca-Cola to become one of the industry’s strongest top-line performers.

The 2025 results perfectly illustrated this strategy. Organic growth reached an exceptional 12%, yet approximately 93% of that growth came from value while only 7% came from volume.

Many companies would have continued following that formula, instead, Coca-Cola recognized its limitations surprisingly early.

Q1 2026 tells a completely different story. Organic growth remained outstanding at around 10%, but this time approximately 80% of the growth came from volume rather than pricing.

The interesting question is not what changed but how it changed.

Portfolio architecture became a penetration tool

Rather than using portfolio management primarily to optimize margins, Coca-Cola increasingly used it to recruit consumers.

The company expanded its pack-price architecture with locally relevant formats capable of addressing different purchasing occasions, affordability needs and retail environments.

Mini cans launched through the convenience channel in the United States provide perhaps the best example. Rather than simply offering a smaller package, they lowered the entry price, expanded affordability, increased impulse purchasing and opened new consumption occasions.

Elsewhere, Coca-Cola introduced locally relevant pack formats, bundled offers, lightweight bottles and country-specific innovations, all designed around one objective: increasing consumer recruitment while maintaining pricing discipline.

The recent launch of Coca-Cola Black follows the same philosophy.

By removing sugar and caffeine while adopting a premium black identity, the company is attempting to create entirely new evening consumption occasions rather than merely competing within existing ones.

Cultural relevance creates consumption occasions

Equally interesting is Coca-Cola’s renewed emphasis on cultural relevance.

Rather than treating marketing as communication alone, the company increasingly uses local culture to create reasons to consume.

Campaigns linked to Ramadan, Chinese New Year, Carnival, March Madness and numerous local celebrations transform the brand into part of culturally meaningful experiences.

One particularly elegant example combines both portfolio architecture and cultural relevance.

The limited-edition mini-can collection celebrating individual U.S. states simultaneously leverages an affordable format while creating collectability, conversation and emotional engagement.

The result is not simply higher awareness, but it is more purchasing occasions and ultimately, more penetration.

Balanced geographical execution

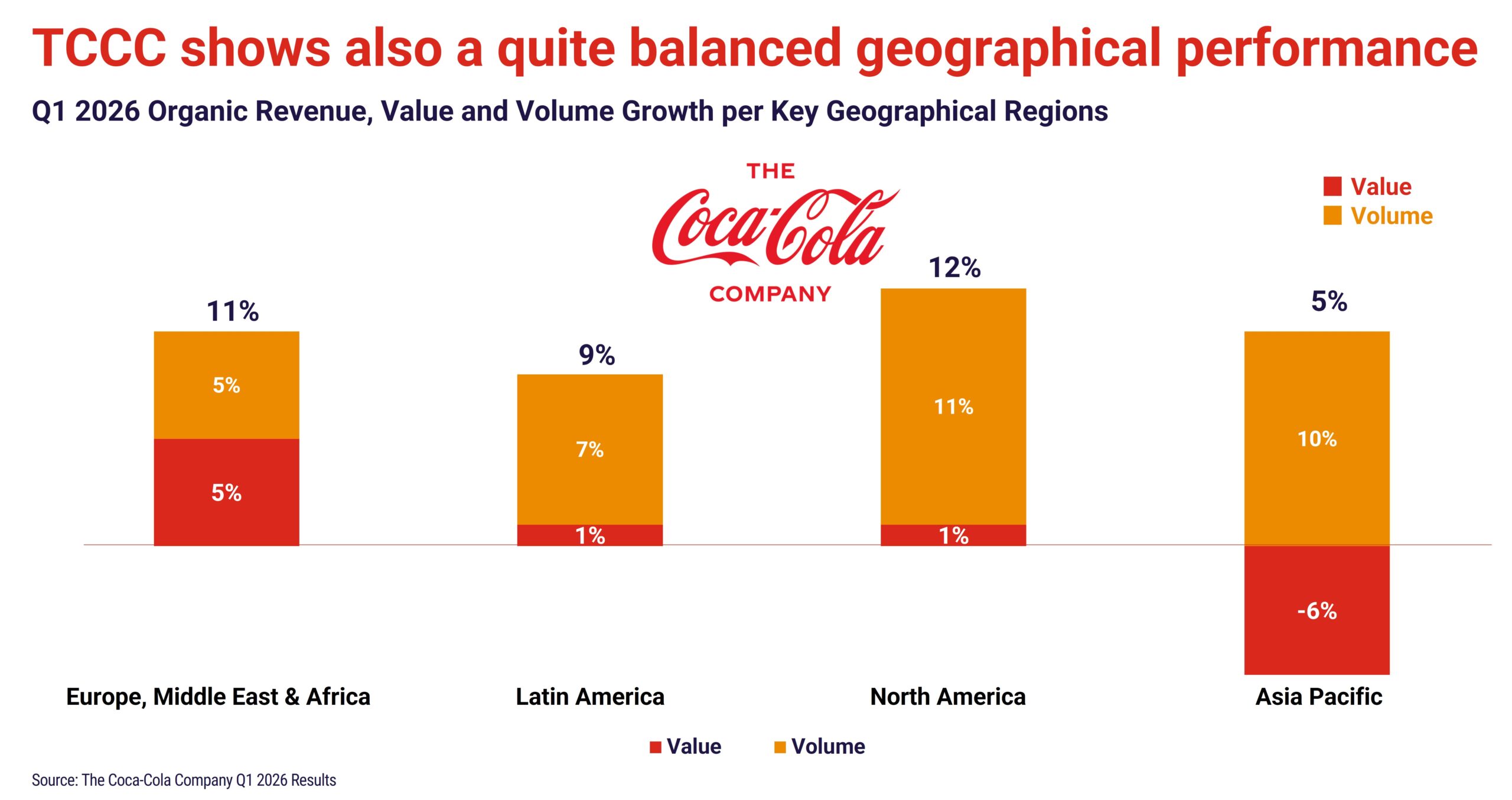

Coca-Cola’s geographical performance reinforces the same lesson. As a Global business the company covers a high number of geographies but with a mix of different brands from the big blockbuster to some more local jewels.

Unlike many competitors, volume growth was broad-based across all four major operating regions, with particularly strong momentum in North America.

This is particularly significant. North America remains one of the most challenging consumer environments globally, characterized by slowing consumption, increasing price sensitivity and intense competitive pressure.

If Coca-Cola can successfully build volume in North America, it demonstrates that penetration growth remains achievable even under difficult market conditions.

Other CPG leaders are reaching similar conclusions

Although each company follows its own strategy, remarkably similar patterns emerge across the quarter.

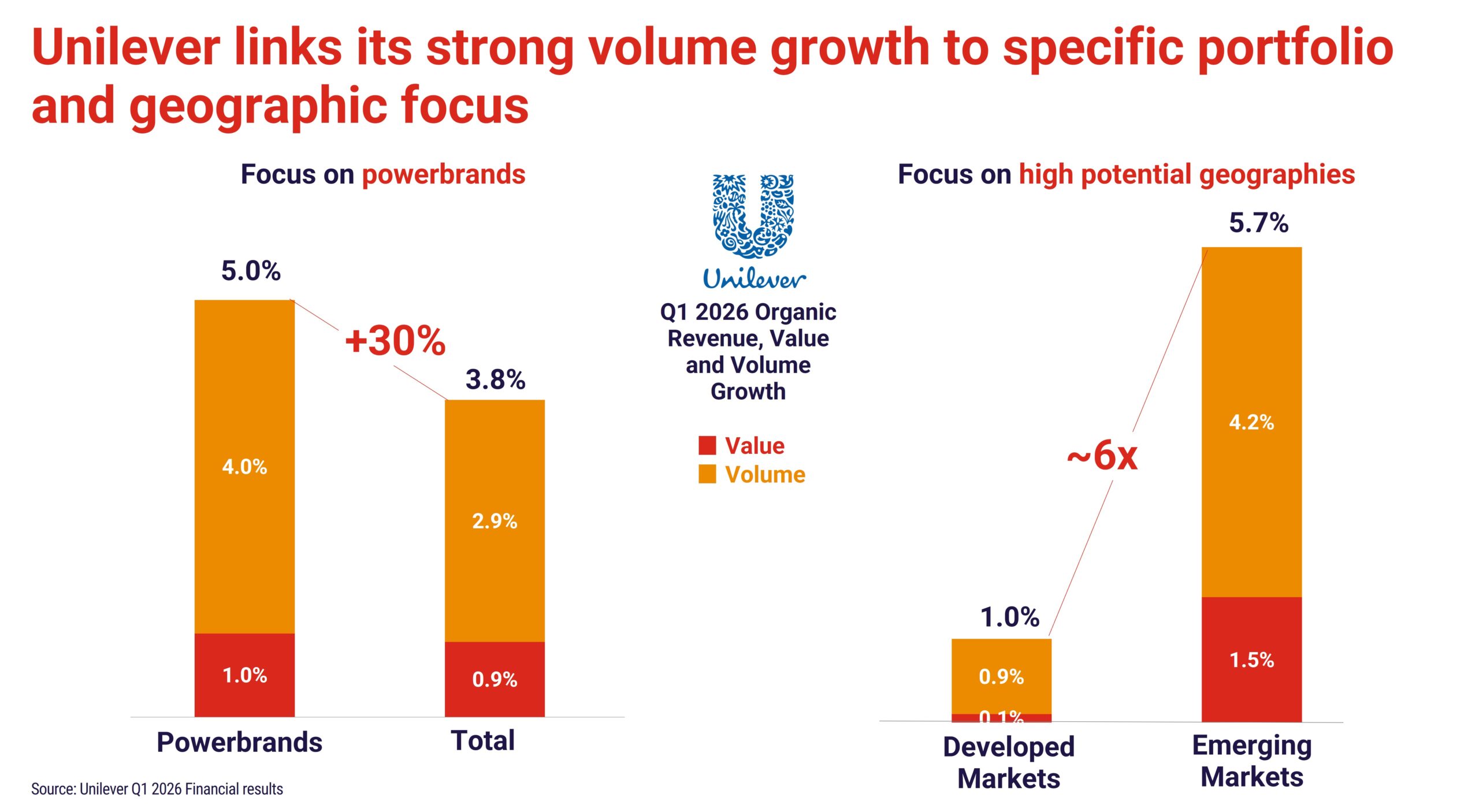

Unilever continues demonstrating the value of disciplined focus. Its strategic decisions to separate Ice Cream and progressively simplify its Foods portfolio are creating a more concentrated business centered on higher-growth, higher-margin categories. At the same time, increased investment behind Power Brands and the company’s strong exposure to emerging markets continue to support balanced value and volume growth. Emerging markets are currently delivering almost six times the growth of developed markets, highlighting the importance of deliberate geographic prioritization.

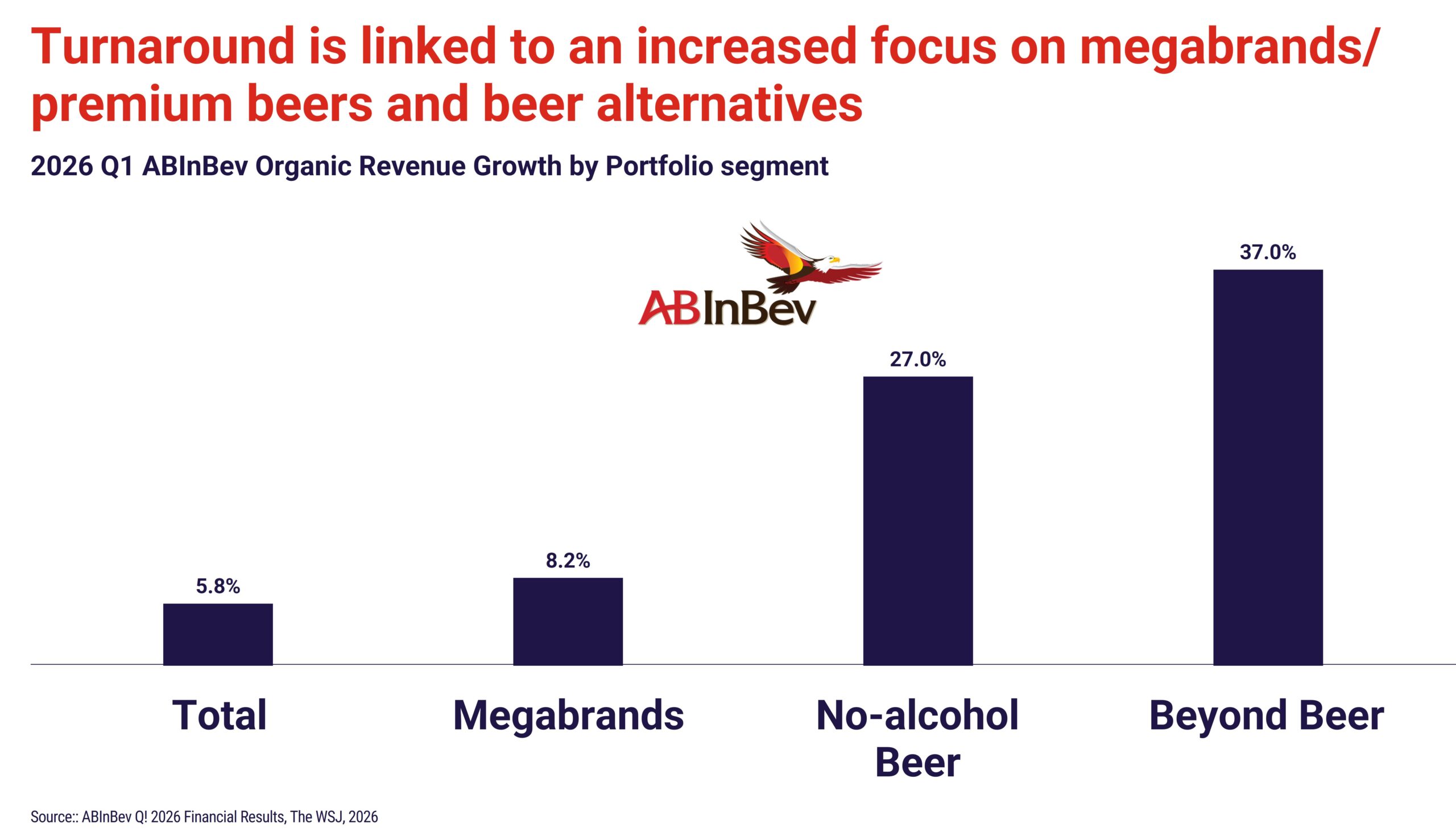

ABInBev perhaps provides the most symbolic turnaround. After eleven consecutive quarters of declining volume, the brewer finally returned to positive volume growth. The recovery appears closely linked to deliberate portfolio choices: stronger investment behind megabrands together with rapid expansion of no-alcohol beer and beyond-beer platforms, both substantially outperforming the core business and capturing entirely new consumer occasions.

Nestlé illustrates another important lesson. Rebuilding volume is an organizational transformation.

Following several years during which pricing became the dominant growth driver, the company progressively lost purchasing occasions across parts of its portfolio as competitors, local brands and private labels expanded their presence.

Re-establishing Real Internal Growth (RIG) as one of the company’s principal strategic metrics went through multiple leadership transitions and several years of changing internal culture and perspective. The encouraging improvement now visible demonstrates that rebuilding penetration demands persistence, organizational alignment and long-term commitment rather than short-term commercial programs.

The beginning of a different growth philosophy

Q1 2026 should not be interpreted as the end of the industry’s volume challenge. One quarter does not reverse several years of structural change.

What it does suggest, however, is that the industry’s largest companies are beginning to rethink the very foundations of growth.

For almost three years, inflation allowed pricing to substitute for penetration. The strategy generated attractive financial performance but gradually weakened consumer recruitment, purchasing frequency and ultimately long-term resilience.

The companies showing the strongest momentum today appear to have recognized that sustainable growth cannot be built on pricing alone. They are making difficult portfolio decisions, prioritizing geographies with the greatest long-term potential, redesigning pack-price architecture and investing in cultural relevance.

Above all, they are placing penetration back at the center of their growth strategies. Because volume does not increase simply because companies decide to sell more products.

Volume grows when companies deliberately create more reasons, more occasions and more opportunities for consumers to choose their brands.

That may ultimately prove to be the most important lesson emerging from Q1 2026.

Turning penetration into a growth strategy

Recognizing that penetration matters is relatively easy. Building a business around it is considerably harder.

Penetration is not the result of one initiative or one successful innovation. It is the outcome of a series of deliberate strategic decisions that determine whether a brand recruits more consumers, creates new purchasing occasions and expands its relevance over time.

This is why, at Sevendots, we developed our Penetration Decision Framework.

The framework helps companies identify where the biggest penetration opportunities lie and, more importantly, which decisions need to be made to unlock them. It provides a structured path to prioritize growth opportunities and align the organization around the choices that matter most across four dimensions:

- Portfolio: Which categories, brands, innovations and pack-price architecture can recruit more consumers and occasions?

- Geographies: Where should investments be concentrated to maximize long-term penetration?

- Channels: Which channels and shopping missions offer the greatest opportunity to expand reach?

- Consumer relevance: How can brands become more meaningful by better addressing evolving needs and local cultural contexts?

The result is not simply a list of growth initiatives, but a clear roadmap that links strategic choices to penetration, volume and ultimately long-term value creation.

The encouraging Q1 2026 results suggest that many leading CPG companies have already started this journey. Those that sustain their momentum will likely be the ones that embed penetration into every major commercial decision—not simply as another KPI, but as the organizing principle behind portfolio, innovation, channel and geographic strategy.

At Sevendots, helping companies make those decisions is at the core of what we do.