Business Strategy 26 May 2026

The Retailer Collaboration Dividend

High-growth retailers are winning through better collaboration with suppliers.

High-growth retailers outperform through stronger supplier ecosystems.

Retail media, agility and supply chain collaboration are now major differentiators.

Sevendots, Singapore

8 minute read

Executive Summary

Retailers that collaborate more closely with suppliers are growing much faster.

That is the headline from brand new research mapping the financial growth rates of retailers against Advantage Group International (AGI) supplier feedback.

The link is especially strong in areas connected to speed, execution, retail media effectiveness, data actionability, cross-functional alignment and supply chain integration.

In other words, the winning retailers are those that are closely working with suppliers where collaboration can be translated into commercial outcomes.

The results show that better collaboration is leading to more investment which is driving better execution which is in turn creating higher growth.

This is what we term the Collaboration Dividend.

Introduction

Across global retail markets, profitable growth is becoming increasingly difficult to sustain.

Retailers are simultaneously managing margin pressure, supply chain volatility, retail media complexity, omnichannel execution challenges, rising consumer expectations, and intensifying competition from both value and digital-first players.

In this environment, scale alone is no longer enough.

The retailers pulling ahead are increasingly distinguished not simply by pricing power, footprint, or negotiating leverage, but by how effectively they collaborate with suppliers.

New analysis across 21 major global retailers combining their financial performance with their supplier collaboration scores (as measured by the global leader in B2B engagement, Advantage Group International) shows that higher-growth retailers consistently outperform lower-growth peers across a broad range of collaboration-related capabilities, particularly in areas tied to retail media execution, agility, data actionability, cross-functional alignment, and supply chain integration.

The implication is significant.

Collaboration is no longer simply a relationship-management exercise or procurement philosophy. Increasingly, it is a structural growth enabler.

The retailers creating the strongest supplier ecosystems are also more likely to move faster, execute more effectively, unlock stronger retail media performance, improve forecasting and availability and translate insight into action more consistently

The evidence is compelling.

In a world where it’s easy to let differences in opinion or strategy get in the way of progress, the strongest retailers are leaning into suppliers and winning through stronger collaboration.

New Research: The Collaboration Gap Between High and Low Growth Retailers

To better understand the relationship between collaboration and retail performance, an analysis was conducted across 21 major retailers spanning grocery, discount, omnichannel, and mass retail formats across North America, Europe, Latin America, Asia, and Australia.

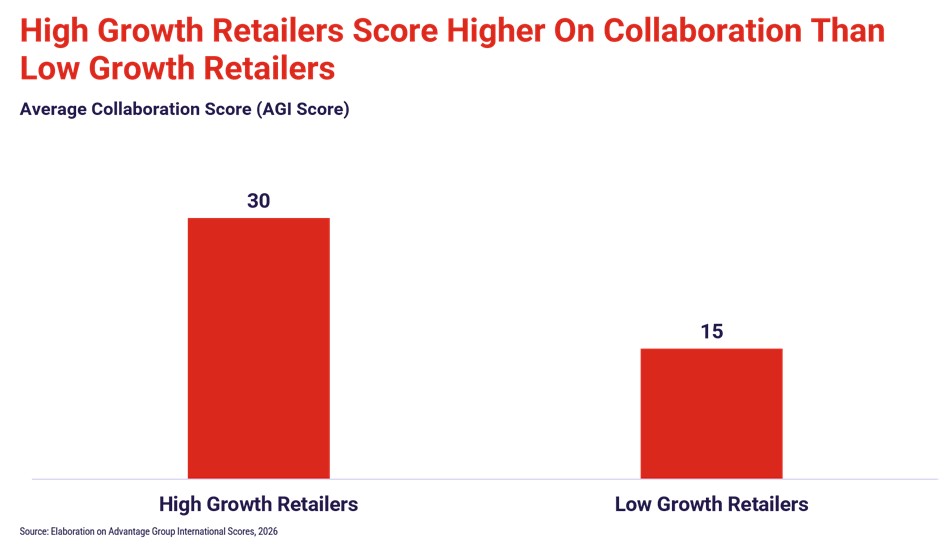

Retailers were segmented into high-growth and low-growth groups using publicly available revenue growth data and a median-split methodology. The winning retailers had an average revenue growth of 4.6% compared to the remainder who declined by 1.2%.

The winners had an average AGI score across all measured dimensions of 30 points, 15 points higher than the rest. A company’s AGI score is derived from anonymous supplier feedback, providing a benchmark of how retailers are viewed by their suppliers in areas like collaboration, service, and value creation.

In other words, the best-performing retailers from a financial perspective were rated significantly better to do business with by their supplier base. For context, 15 points difference is a highly significant number and shows that being more collaborative pays off with real commercial results.

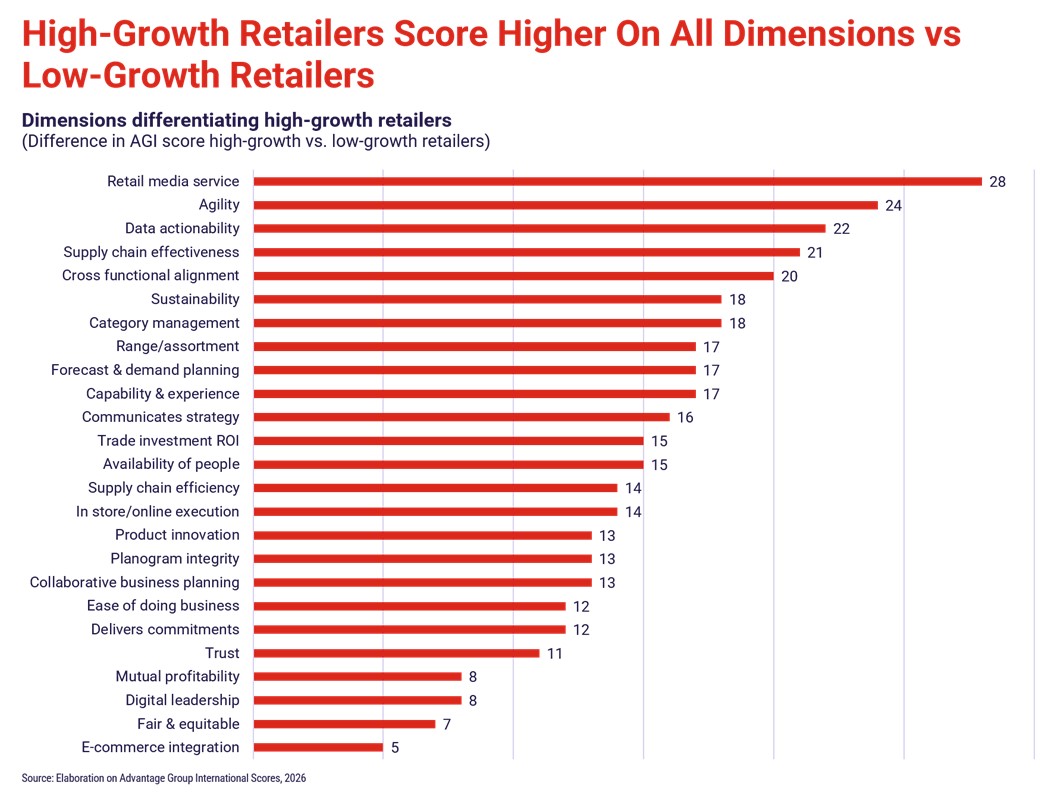

Strikingly, high-growth retailers score better across every measured capability.

However, as the visual below shows, the real separation appears in a relatively small number of commercially critical areas where the gaps are extremely large.

The strongest performing retailers consistently outperform lower-growth peers in capabilities tied directly to retail media monetization, speed and agility, data activation, supply chain collaboration, cross-functional alignment, category and assortment execution.

These are not soft relationship indicators, they are increasingly the operational systems that determine how quickly retailers can respond, align, execute, and grow.

Viewed together, the findings suggest that collaboration increasingly acts as a multiplier across the broader retail operating model.

Retail Media Has Become The Biggest Point of Separation

The single largest performance gap between high and low-growth retailers appears in retail media capability. We commented on the rising power of retail media in our recent article from Colin McAllister (The Rising Power of Retail Media).

High-growth retailers outperform lower growth peers by 28 points in retail media — the largest gap observed across the entire analysis.

This is particularly significant because retail media is no longer simply about advertising product. Increasingly, it sits at the intersection of supplier investment, category growth, omnichannel activation, data monetization and digital execution.

The strongest retailers are not simply treating retail media as an isolated profit stream, instead they are integrating media into broader category, assortment, and shopper-growth strategies. As such, suppliers working with these retailers are more likely to experience clearer ROI measurement and better alignment between media and execution which in turn gives them greater confidence in investing.

By contrast, lower-performing retailers are more frequently perceived as operating fragmented retail media ecosystems where execution, insight, and commercial objectives remain disconnected.

High-growth retailers are more thoughtfully building out their teams and offerings in this space and consistently appear better able to help suppliers understand:

- Where to invest

- Why to invest

- How value will be created

- How performance will ultimately be measured

This matters because supplier investment increasingly flows toward retailers capable of demonstrating measurable commercial return.

Speed and Data Are Emerging As Competitive Multipliers

The next major point of separation is operational agility.

High growth retailers outperform lower growth peers by 24 points in agility and 22 points in data actionability. These are not simply operational metrics, they reflect how effectively organizations convert insight into execution.

In practice, suppliers describe high-performing retailers as organizations that make decisions faster, align teams more effectively, respond more quickly to changing conditions, translate data into action with greater consistency and remove friction from execution.

This matters because retail complexity is increasing rapidly.

Promotional cycles are shortening. Consumer behavior is fragmenting. Omnichannel execution is becoming harder. Supply chains remain under pressure.

In this environment, the ability to act quickly increasingly becomes a growth advantage in itself. Retailers that move slowly often create hidden execution costs for suppliers, even when strategic intent is strong.

By contrast, high-growth retailers appear better able to align commercial, supply chain, media, and category functions around shared priorities, allowing decisions to move more efficiently from insight to action.

Communication also plays a major role, with high-growth retailers outperforming lower-growth peers by 16 points in communicating strategy. Suppliers working with these retailers typically describe greater clarity of direction, faster organizational alignment, better visibility into priorities and more confidence in long-term planning

Taken together, these capabilities create faster and more coordinated ecosystems.

And increasingly, speed itself appears to be becoming a source of competitive advantage.

Supply Chain Excellence Is No Longer Just About Cost

One of the most consistent findings across the analysis is the strength of supply chain-related collaboration among higher-growth retailers.

High-growth retailers significantly outperform lower-growth peers across supply chain effectiveness and efficiency, as well as forecast and demand planning.

This is a big shift as historically, supply chain discussions were often centered around cost reduction whereas today, the role of the supply chain is expanding.

Leading retailers increasingly treat supply chain collaboration as a shared growth system with suppliers rather than a downstream operational process.

Which is why suppliers working with high-growth retailers consistently report earlier visibility into demand shifts, better forecasting alignment, faster issue resolution, greater transparency, fewer late-stage surprises and more reliable execution.

These capabilities matter commercially because they directly impact on-shelf availability, promotional effectiveness, inventory optimization, waste reduction and shopper satisfaction.

In increasingly volatile retail environments, supply chain collaboration is becoming a competitive advantage rather than simply an operational necessity, and the retailers that execute best increasingly appear to be those that treat suppliers as integrated operating partners rather than external vendors.

Organization Alignment Is A Hidden Driver

Another important finding from the analysis is the importance of organizational alignment, as evidenced by the fact that high-growth retailers significantly outperform lower-growth peers in cross-functional alignment, capability and experience, availability of people and collaborative business planning

Retailers with strong internal alignment also typically make it easier for suppliers.

Easier to access the right decision-makers.

Easier to resolve issues quickly.

Easier to align around shared objectives.

Easier to coordinate across functions.

Easier to translate plans into execution.

This becomes particularly important as retail operating models become more interconnected across different channels and formats.

In complex environments, alignment itself becomes an efficiency advantage.

Trust Matters But It No Longer Differentiates Leaders

It is also notable that traditional relationship-health measures such as trust and fairness show smaller gaps than more execution-oriented capabilities.

This does not mean these factors are unimportant but rather, it suggests they have increasingly become baseline expectations.

High-growth retailers still outperform lower-growth peers on trust, however, the separation is materially smaller than in areas such as retail media, agility, or data actionability.

Trust is necessary, but no longer sufficient in itself.

Instead, retailers increasingly differentiate themselves by combining strong relationships with superior execution, speed, and commercial sophistication.

What High Growth Retailers Do Differently

Viewed collectively, the analysis suggests that high-growth retailers tend to behave differently in several important ways.

They are more likely to treat suppliers as strategic growth partners rather than purely commercial counterparties, use data collaboratively rather than transactionally, integrate retail media into broader growth strategies, move quickly from insight into execution, build transparent and responsive supply chains, align internal functions around shared priorities and create clearer commercial outcomes for suppliers.

Importantly, these behaviors compound over time and as collaboration improves then supplier trust increases, execution improves and investment confidence grows.

Over time, this creates a widening separation between retailers operating collaborative ecosystems and those operating more transactional models.

Let’s look at three examples of retailers that focus on collaboration as a competitive advantage.

Walmart: Collaboration Governance

Walmart stands out for turning collaboration into a structured operating rhythm, with suppliers consistently describing strong joint business planning, disciplined execution, high operational rigor and advanced supply chain coordination.

Rather than depending on individual relationships, the governance, systems, and cadence create an ecosystem where suppliers can align more quickly and execute more consistently at scale.

Amazon: Systems And Commercial Sophistication

Amazon’s strength lies in its combination of platform scale, retail media sophistication, logistics capability, automation and data infrastructure.

Suppliers consistently view Amazon as one of the most commercially advanced retail ecosystems globally with its retail media capabilities in particular being frequently cited as industry-leading due to sophisticated targeting, closed-loop measurement and rapid optimization.

Transparency and commercial effectiveness are key elements of their collaborative value creation.

Tesco: Strategic Consistency

Suppliers consistently describe clear strategic alignment,

strong cross-functional access, reliable execution, reciprocal data sharing and structured planning cadences.

This matters because it reduces friction and increases execution consistency at scale.

The result is that suppliers often experience Tesco as a retailer where plans move more predictably from strategy into in-market execution. That consistency increasingly appears linked to Tesco’s sustained competitive performance.

Conclusion: The Winning Retailers Are Not Winning Alone

There are two really critical findings from this work.

First, winning retailers are collaborating more openly with their suppliers.

They fundamentally believe it is important, they talk about it, they measure it.

Secondly, collaboration increasingly appears tied to capabilities that directly influence growth. The largest gaps between high- and low-growth retailers are not in traditional relationship measures alone but in areas connected to speed, execution, retail media effectiveness, data actionability, cross-functional alignment and supply chain integration.

In other words, the retailers pulling ahead are increasingly those that have built organizational systems capable of translating collaboration into commercial outcomes.

This matters because suppliers increasingly make strategic choices around investment prioritization, resource allocation, innovation support, data sharing, commercial collaboration and talent deployment.

Retailers that create stronger collaborative environments are therefore increasingly likely to attract disproportionate supplier focus and investment.

This is what we call the Collaboration Dividend.

And it is a winning strategy for retailers.

At Sevendots, we help brands unlock pathways to volume growth, which includes building the right brand and category plans in close collaboration with your retailer partners. Our team has extensive senior sales, strategy and marketing expertise, gained through experience working within many of the largest CPG companies around the world. Reach out to us if you are looking for support to drive out-sized growth in 2026 and beyond.