Brand Growth, Portfolio Management 05 March 2026

Private Labels: From Alternative to Structural Growth Engine in CPG

Private Labels are no longer a marginal or cyclical phenomenon in CPG.

Private Labels follow a consistent global pattern; markets are simply at different stages.

Growth accelerates where penetration is low and now spans both affordability and premium tiers.

Consumer perception of Private Labels has fundamentally changed: they are now chosen for both value and quality.

Sevendots, Milan

7 minute read

What does the future of Private Label look like?

There is no shortage of talk around Private Labels right now, and for good reason.

They have become the elephant in the room for the entire CPG industry.

When Private Labels first started to appear in a more structured way on supermarket shelves, their impact was clearly disruptive. Over time, many brand owners assumed they would eventually reach a natural ceiling (much like discounters did) within specific geographies and categories and settle into a defined but stable role in the market.

The reality is proving very different.

Private Labels have recently regained growth momentum, expanding across geographies and new categories. In several markets, they already command well over half of category sales, and their trajectory suggests they are not done yet in further expanding. While a few categories in specific countries show signs of Private Label penetration plateauing, allowing major brands to regain momentum, Private Labels are increasingly moving from the margins to the very center of the market.

This shift has fueled a wave of provocations.

One recent example is a LinkedIn post by Juan Viñas featuring a fake Financial Times cover titled “Procter splits from Gamble”, mocking a scenario in which the company separates into two entities: one continuing to sell branded products, the other focusing exclusively on producing Private Labels for retailers. Another provocation projects Private Label share reaching 100% of the market by 2040.

These scenarios are intentionally exaggerated, but they resonate because they tap into a real underlying anxiety.

What the data clearly shows is this:

Private Labels are here to stay, and they are hungry to expand their space. For branded manufacturers, the question is no longer whether Private Labels matter, but how to compete, differentiate, and remain relevant in categories where they are structurally embedded.

This is the context in which the following analysis should be read.

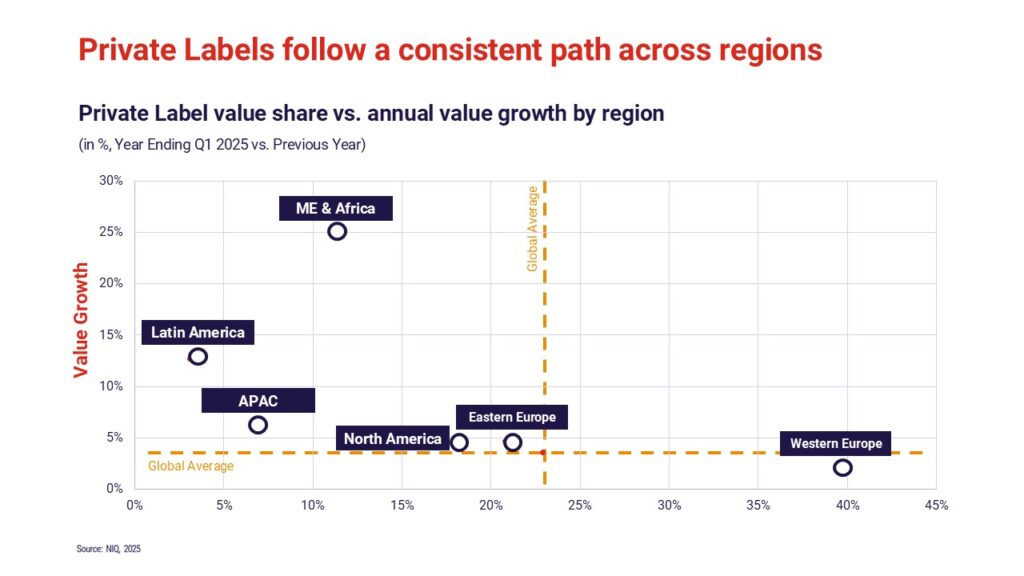

Private Label growth follows a consistent global pattern

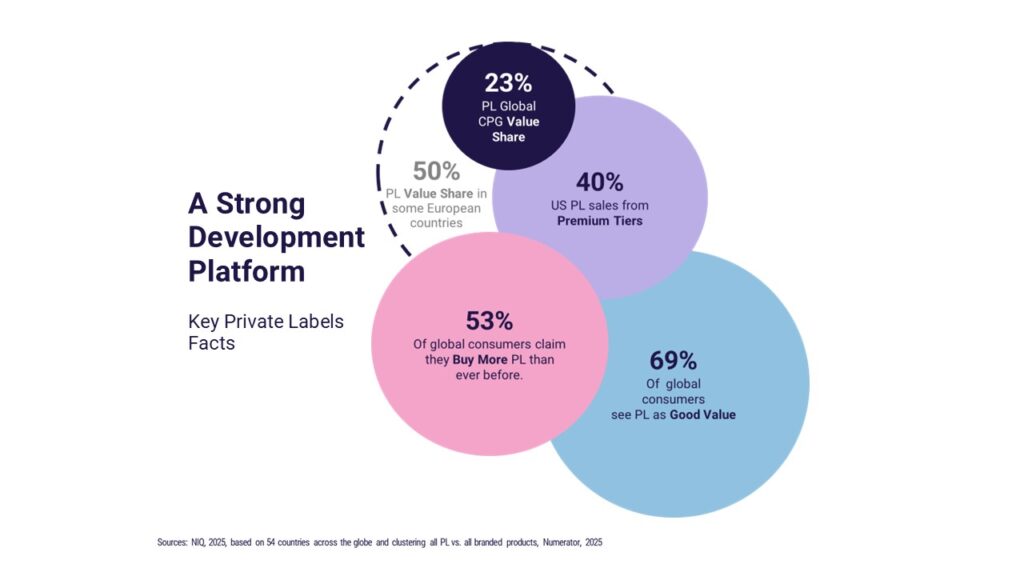

At a global level, Private Labels account for roughly 23% of CPG value, but their penetration varies widely by geography. What is striking, however, is not the disparity itself, but the consistency of the trajectory.

Where Private Label share is still low, growth is rapid.

Where share is already high, growth is naturally moderating, but penetration remains structurally strong.

Regions are not following different models; it looks like they are simply at different stages of the same journey, driven by the development both within grocery channels and discounters such as Aldi and Lidl.

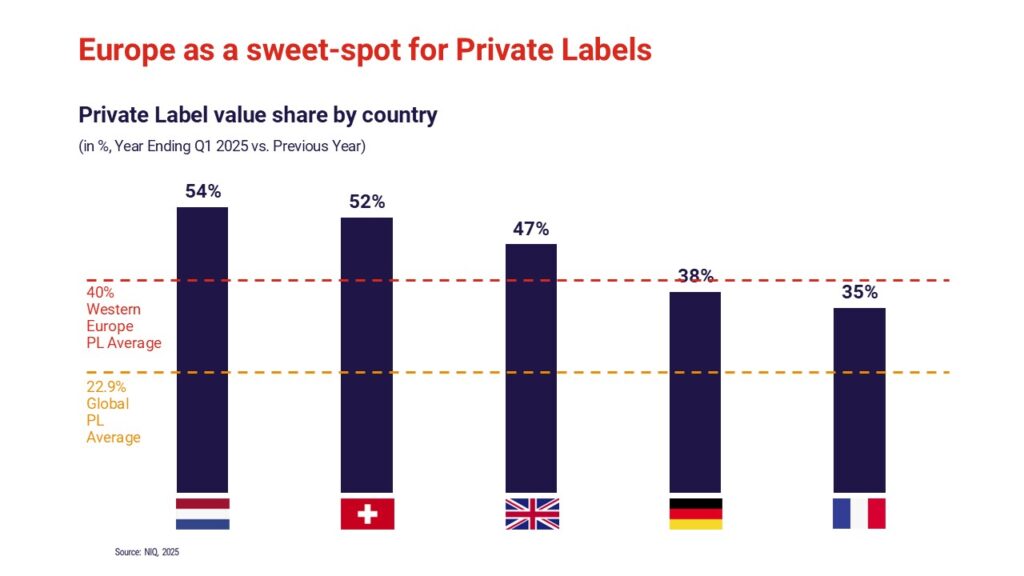

Europe signals the structural end point of Private Label

penetration

Europe provides the clearest picture of where this journey leads. Based on Europanel data across 12 European countries, more than half of shoppers regularly buy Private Labels, and almost 30% exclusively buy Private Labels within specific categories, a figure that has continued to grow since 2021.

In markets such as Switzerland, the Netherlands or the UK, Private Labels are no longer perceived as an alternative to brands, they are themselves brands and the default choice for many consumers. This reflects a deep behavioural shift, not a temporary affordability response.

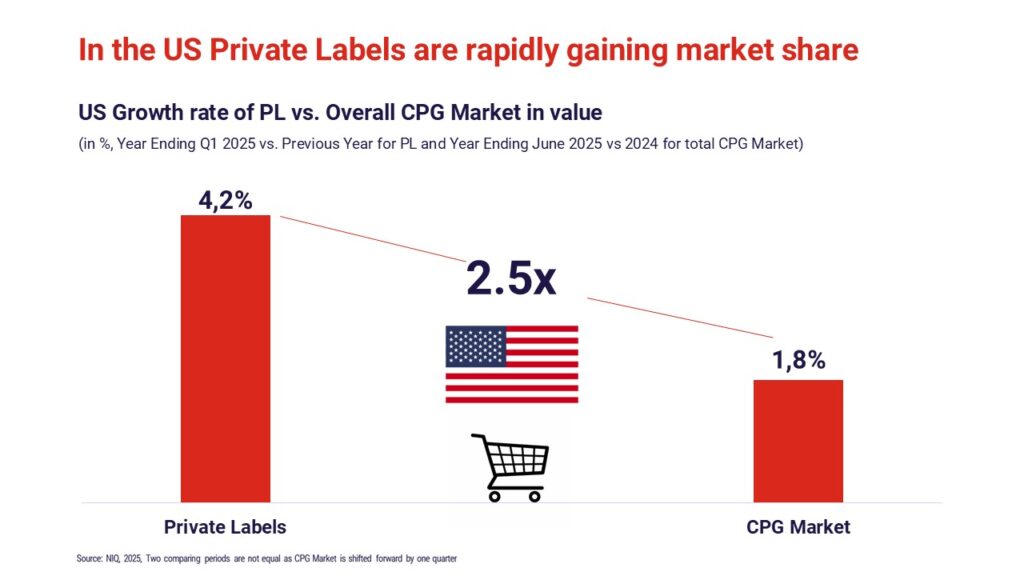

Growth accelerates where penetration is still low

The speed of Private Label expansion is highest in markets that are still catching up. The United States is a clear example in recent years (with Asia and Latin America likely to follow in coming years).

In the United States, Private Label growth is fueled by consumer polarisation:

- consumers under pressure turn to Private Labels for affordability,

- while more affluent consumers increasingly adopt premiumised Private Label offers.

Today, close to 40% of U.S. Private Label sales already come from premium tiers, highlighting that Private Labels are expanding across the entire value spectrum.

Walmart is just one of the many retailers which stretched their Private Label portfolio to cover the whole spectrum from value tier to real premium products.

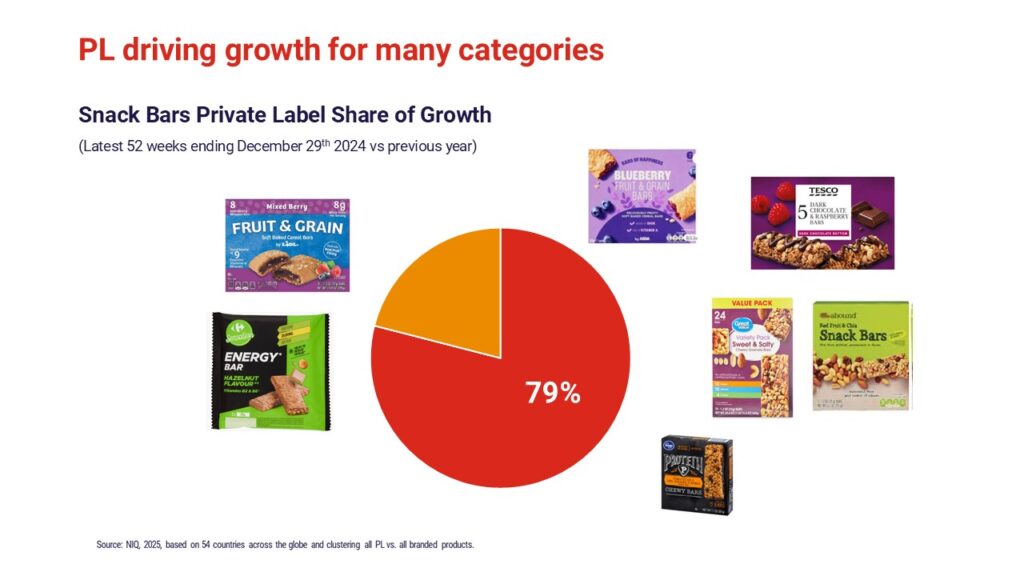

Private Labels don’t just take share, they grow categories

Another critical shift is how Private Labels contribute to category growth. Increasingly, their role goes beyond price competition.

Retailers are using Private Labels to strengthen their own equity by:

- move faster on trends,

- introduce innovation at scale,

- and expand consumption occasions.

A clear example is the UK, where Lidl was among the first to launch a Dubai Chocolate snack bar, ahead of traditional branded manufacturers. This ability to combine speed, relevance and accessibility allows Private Labels to stimulate category growth, not just redistribute share.

In March 2025 Lidl launched its own-label Dubai Style chocolate bar through an extremely successful social media shopping initiative on TikTok. This built the foundation for the roll out of the bars in all Lidl stores.

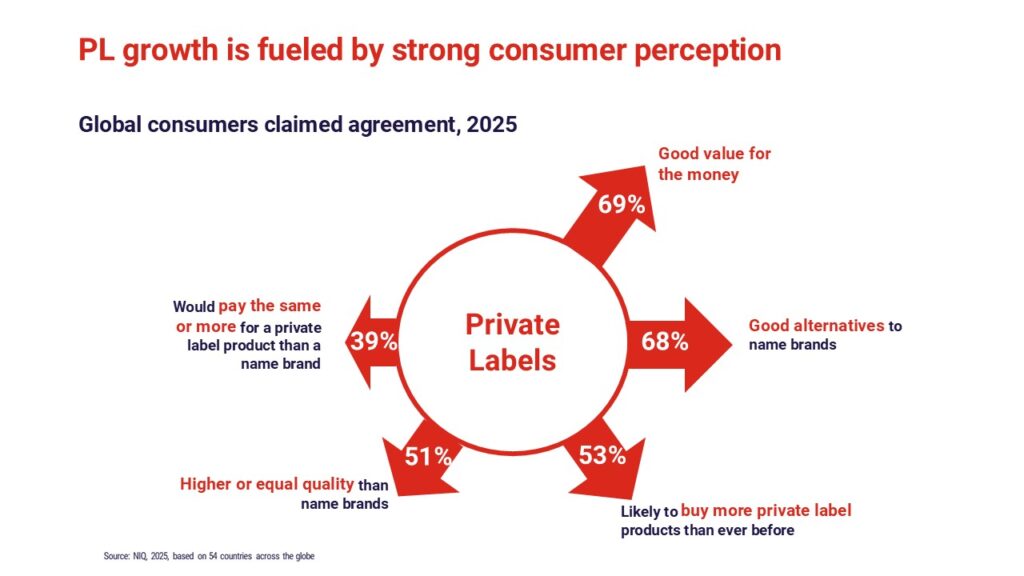

Consumer perception has structurally shifted

Ultimately, Private Label momentum is underpinned by a profound change in consumer attitudes.

Globally:

- nearly 70% of consumers see Private Labels as good value for money,

- two thirds consider them good alternatives to branded products,

- over half believe their quality is equal or superior versus branded products,

- and a growing share is willing to pay the same, or even more, than branded products for

Private Labels.

Private Labels are no longer chosen despite being Private Labels, but increasingly because they are.

What happens next? Two structural scenarios

As stated, Private Label share continues to expand across markets. Portfolios now span from entry price to premium and super-premium. Household penetration is rising and consumer trust has structurally improved.

From here, two structural forward-looking dynamics are most likely:

- Portfolio Expansion – Premium Private Label accelerates

The most dynamic expansion is no longer at the entry tier but at the top.

Retailers are successfully building premium and experience-led Private Label ranges, capturing higher-margin segments once dominated by branded manufacturers. If this continues, value growth will increasingly be co-driven by retailer-owned brands, compressing the mid-tier and intensifying competition around differentiation.

- Structural Integration – Retailers integrate further

As Private Labels scale, retailers gain margin, data, and negotiation power. The next logical step is deeper integration based on tighter supplier partnerships, greater control over innovation pipelines, and stronger direct sourcing capabilities.

In this scenario, retailers evolve from distributors into orchestrators of the value chain.

Competition shifts from shelf space to structural control of the value chain.

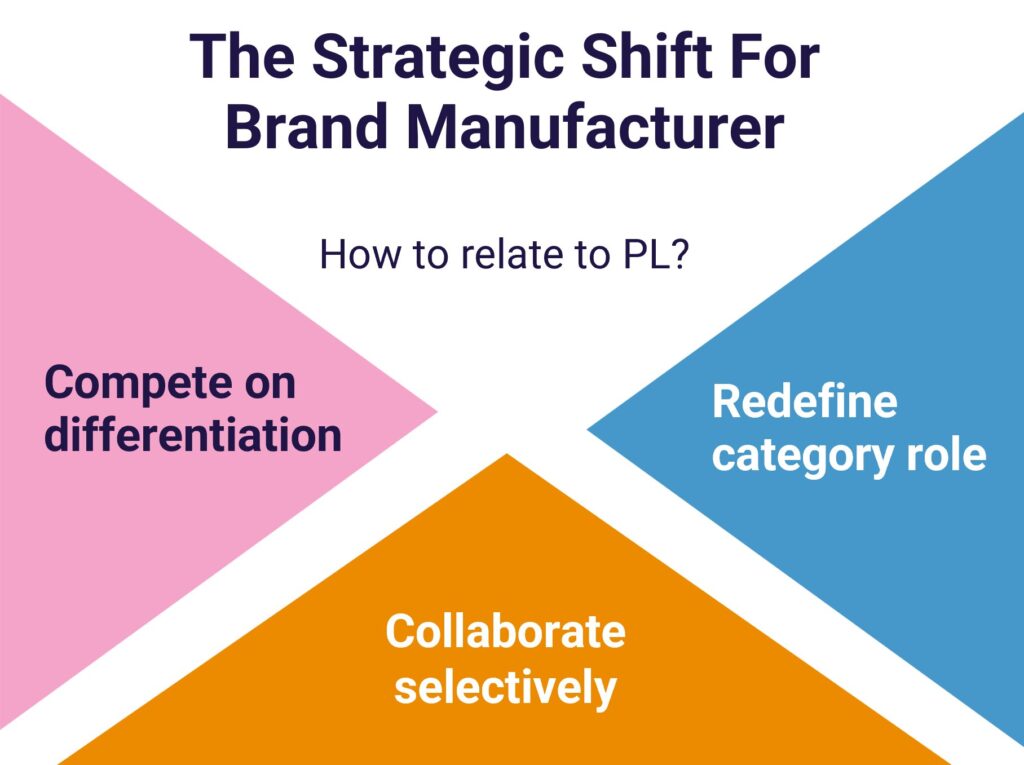

What does this mean for branded players?

The rise of Private Labels reflects structural changes in value perception, retail power, and consumer behavior.

For branded manufacturers, the strategic question is no longer whether Private Labels will continue to grow, but which strategic posture to adopt in response.

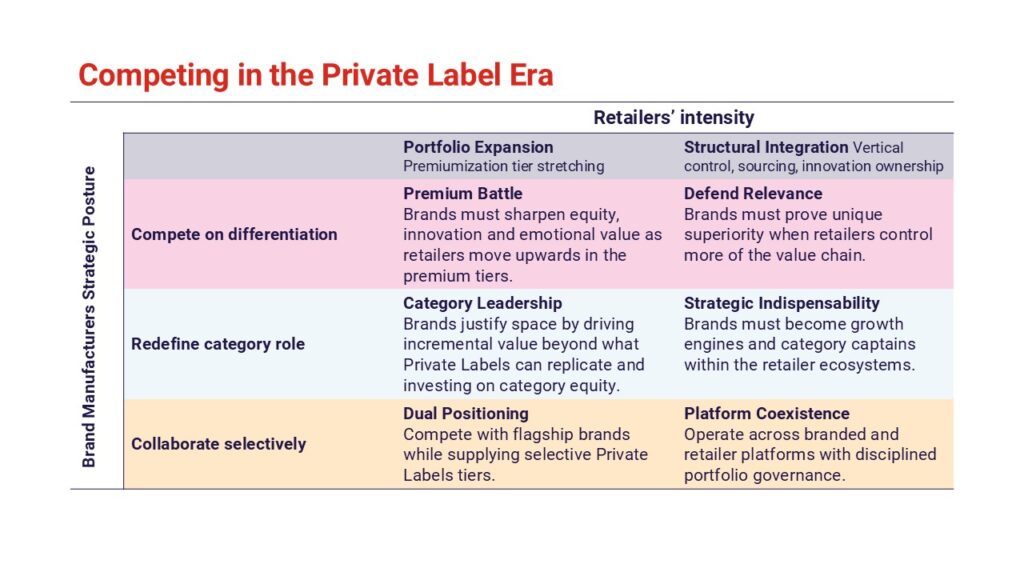

There are three main strategic options for Brand Manufacturers:

- Compete on differentiation

Brands must win where Private Labels cannot easily replicate value. This requires radical clarity in positioning, stronger emotional equity, distinctive innovation, and visible superiority that justifies a price gap. Incremental improvements are not enough. The brand must stand for something unmistakable, and deliver it consistently.

- Redefine category role

Brands must move beyond product competition and elevate their strategic relevance. This means driving incremental category growth, shaping consumption occasions, and proving their contribution to total value creation. The objective is not just to hold share, but to become indispensable in the category architecture.

- Collaborate selectively

Brands must adopt a portfolio mindset. Competing where they have structural

advantage, while selectively partnering where scale, capabilities, or economics justify it. Collaboration is not a retreat, it is a strategic choice that must einforce long-term value, protect core equity, and strengthen overall competitive positioning.

There is already early evidence that strategy makes a difference.

In Europe, branded manufacturers are managing to regain share in categories where the perceived value gap remains meaningful and packaging differentiation is clear.

Between 2021 and 2024, Private Labels grew from 29% to 33% in categories where they were underpenetrated. However, in categories where they already held 36% share, penetration slightly declined to 34%.

This suggests a potential ceiling effect in highly saturated segments and reinforces that differentiation still matters. Private Label growth may be structural, but it is not automatic in every category configuration.

Strategic imperatives going forward

The evolution of the market will depend on how these forces interact.

If Private Label accelerates across premium tiers, differentiation becomes decisive. If retailers deepen structural integration, brands must either elevate their category role or integrate selectively into retailer ecosystems.

Most manufacturers will not choose a single posture. They will operate across all three, depending on category dynamics, retailer concentration, and competitive intensity.

The winning approach will be deliberate, portfolio-based, and retailer-specific.

What is no longer viable is passive defense. Private Label is now part of the structural architecture of CPG.

Strategic clarity, not reaction, will determine who continues to create disproportionate value and benefit from it in the long term.

Sevendots Sevendots help brand owners move beyond defensive responses, redefining where and how their brands can win in categories reshaped by retailer power and consumer expectations.

We support manufacturers in:

- sharpening brand and portfolio differentiation where Private Labels are strongest,12

- identifying the growth pockets that still matter to consumers,

- and reinforcing their role as credible category partners, capable of sustaining category captainship and creating value in retailer interactions.

If you’re reassessing how your brands compete, and lead, in categories where Private Labels are structurally embedded, we’d be happy to exchange.